Soufflet Analysis: Factors of the World Wheat Crop Reduction

The Latifundist.com journalist has recently gone on the agrarian Tour de France accompanied by the key clients of Soufflet Agro Ukraine. At the headquarters of the Soufflet Group, which is France's largest private grain trader, the company presented its forecasts on the development of the situation in the global and regional wheat markets. We are sharing the French experts` analysis on the fundamental and seasonal factors that will shape the situation in the grain market.

The wheat yield will be lower

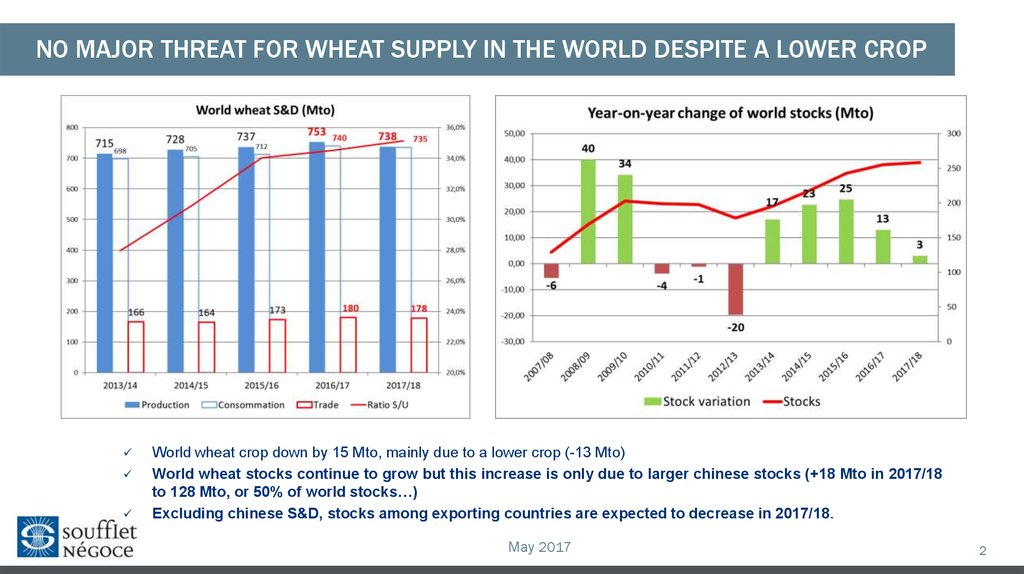

According to the company analysts` expectations, world wheat production will decrease by 15 million tons to 738 million tons compared to 753 million tons last season. However, experts do not see threats for deliveries to grain-deficit regions, due to the growing carryover stocks among other factors. This year, they totaled 128 million tons. The increase of 18 million tons is primarily due to Chinese reserves.

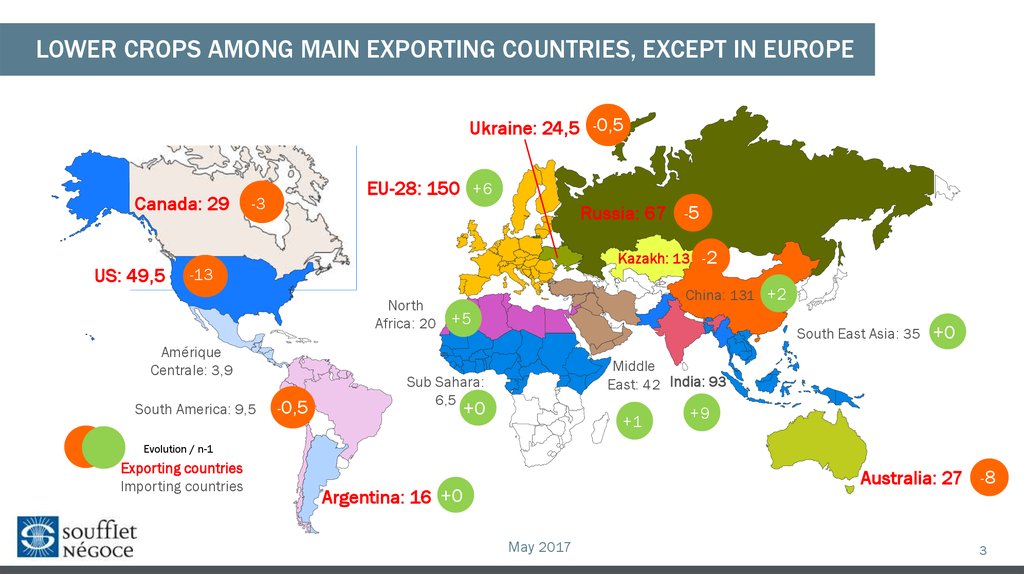

The availability of large carryover stocks in a number of countries could have a negative impact on prices. However, the wheat yield is expected to decrease in the major grain-producing regions in the current season, which helps to maintain the price balance. Among the producers of the Black Sea region, Russia can demonstrate a decrease of 5 million tons, Kazakhstan - 2 million tons, Ukraine - 0.5 million tons. The biggest decline is expected in the North American region.

North hemisphere

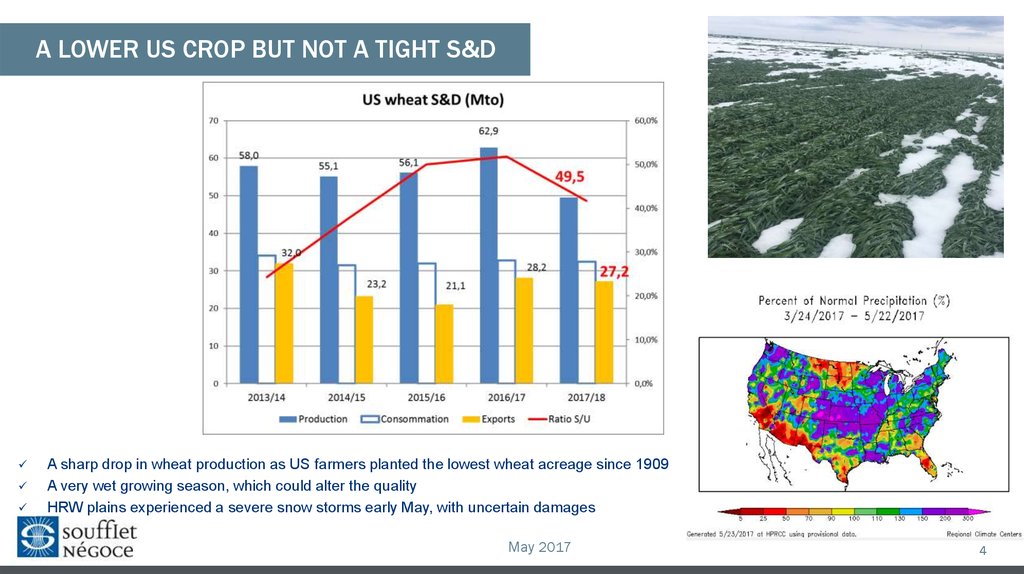

This year American farmers have sown the smallest areas of wheat since 1909. In the US, 13.1 million hectares of winter wheat were sown, which is 1.5 million hectares less than in 2016. At the same time, the crop of HRW-wheat decreased by 2.17 million hectares (-12%), SRW-wheat by 140 thousand or by -6% and WW-wheat by 56 thousand hectares or (-4% ).

According to the latest USDA reports, the output of various wheat varieties has demonstrated a deeply negative value compared to the same period last year: from -11% to -31%.

Snowstorms and windstorms followed by a very humid vegetation period can have a negative impact on the quality and quantity of the crop. In general, in the current season in the US, the gross wheat yield is expected to reduce by 13 million tons to 49.5 million. At the same time, Americans will still hold an active place in the market due to large reserves of the past year.

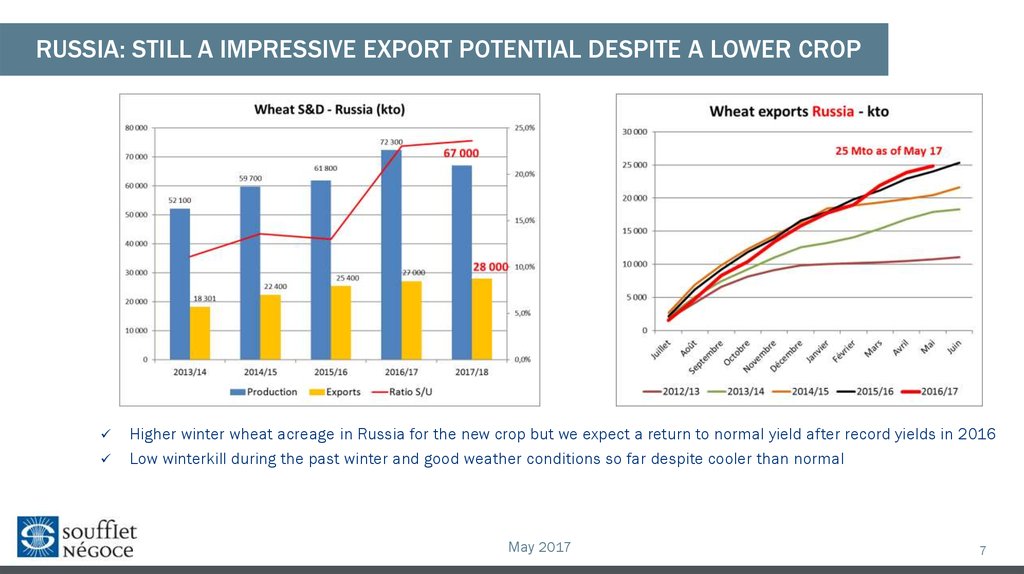

The Black Sea region will remain the main export region of wheat. In Russia, more areas for winter crops have been allocated, but experts expect a certain decrease in the harvest (by 5 million tons) to 67 million tons after a record yield in 2016.

At the same time, the export of wheat from the Russian Federation may exceed the last year level by 1 million tons and amount to about 28 million tons.

The key markers for the possible change in the volumes of Russian exports are the ratio of ruble to dollar, the agreements of the Russian Federation with the main importing countries, for example, Turkey, which closed the market, as well as the policy of internal grain interventions conducted by the Russian government.

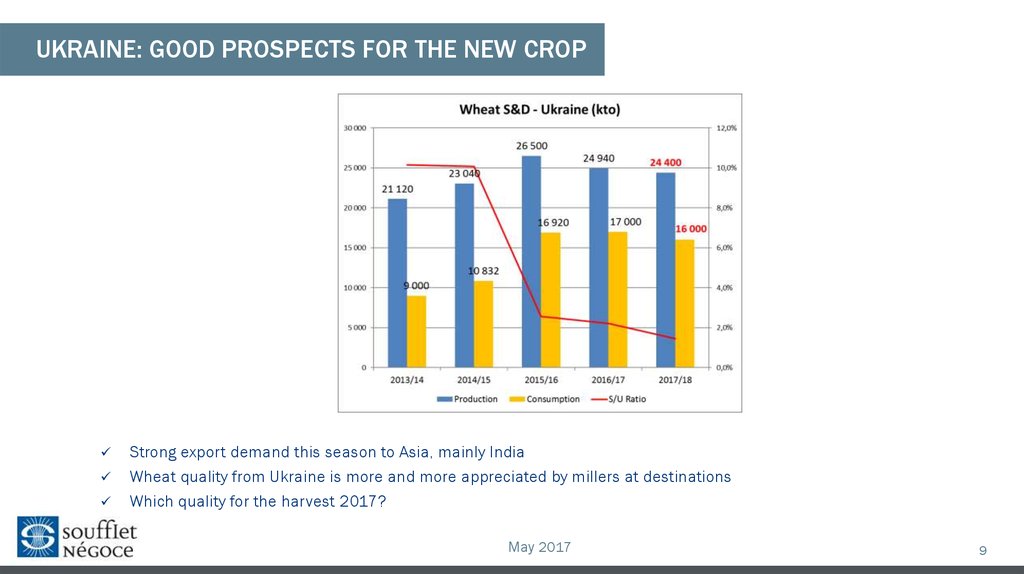

According to the current expectations of Soufflet analysts, the production of wheat in Ukraine will decrease by 0.5 million tons and amount to 24.4 million tons. The prospective export volumes are estimated at 16 million tons against last year's 17 million. At the same time, the quality of Ukrainian wheat is increasingly valued in the world market . While Russian grain is mainly delivered to the North African region, Ukrainian wheat mostly goes to Asian regions, such as India.

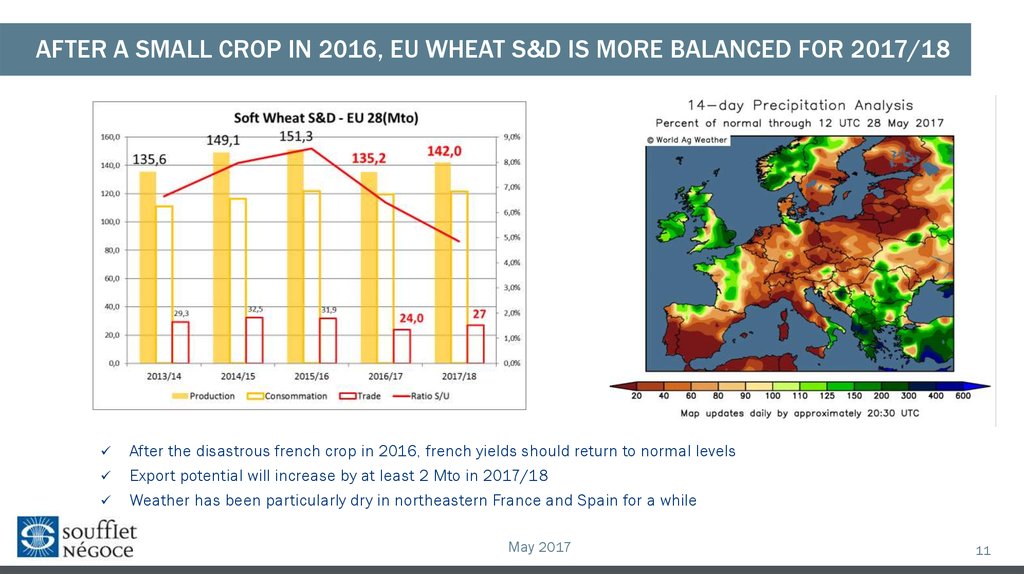

In the EU experts expect the wheat yield to grow and return to a stable level of 142 million tons from last year's 135.2 million, formed due to the extremely low harvest in France.

A spring drought in the north-east of France and in Spain caused a certain concern. Nevertheless, the current forecast implies an increase in the EU export potential by at least 2 million tons.

Southern Hemisphere

The reform, carried out by President of Argentina Mauricio Macri, implying the abolition of the wheat export duty, led to the fact that the area for this crop has grown by 50% in this country since December 2015. In the season of 2017-2018, the yield is expected to reach 17 million tonnes with maintaining last year's export level of 10 million tonnes.

However, the devaluation of Peso gives another powerful push to increase grain production and export volumes. At the same time Argentine grain is present on the market for three months from December to February, and they can be very aggressive during this period.

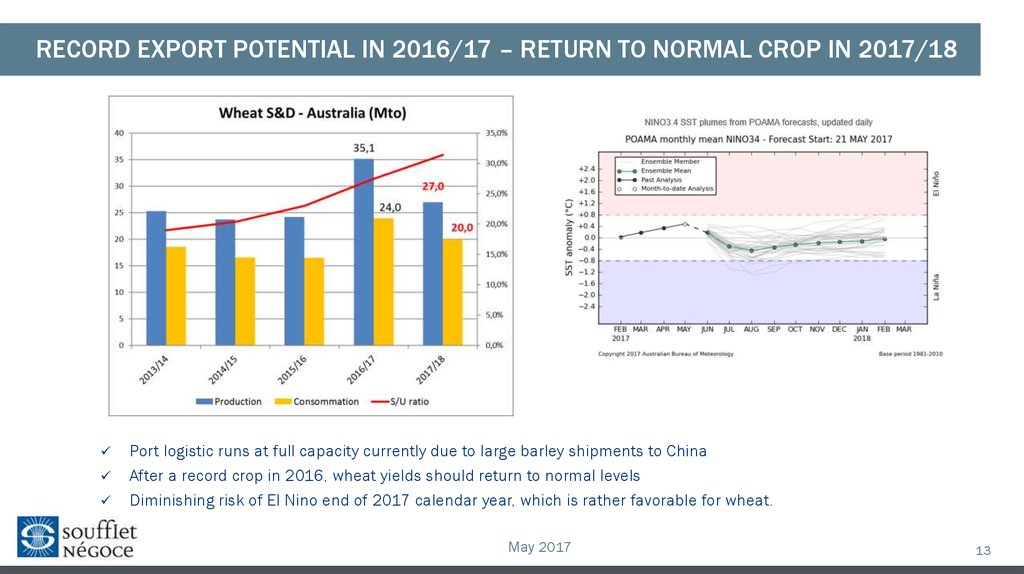

The gross harvest is expected to decrease by 8 million tons to 27 million tons in Australia after a record harvest last year. Export will decrease by 4 million tons.

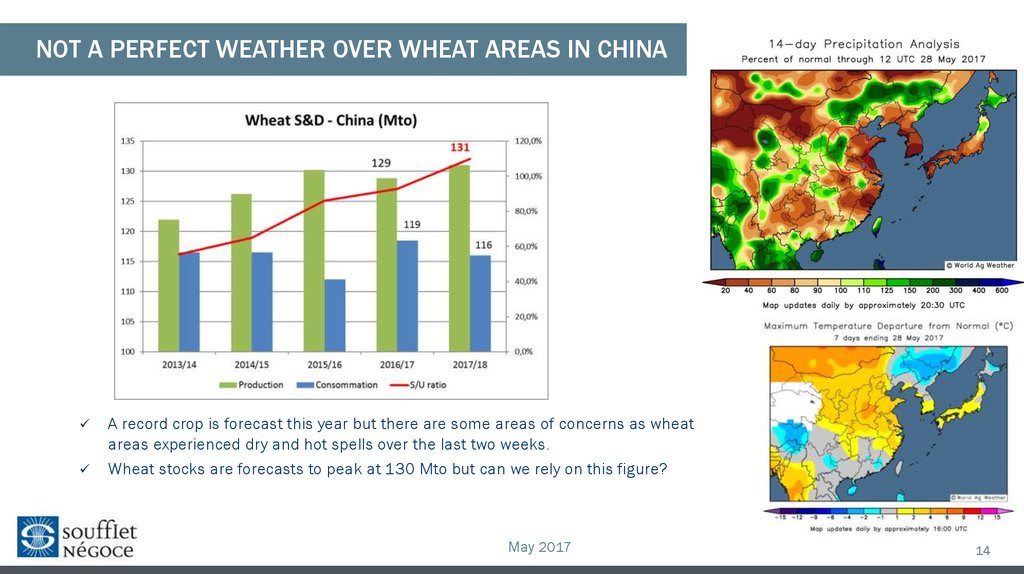

A record wheat yield of 131 million tons is expected in China. The figures may be lower due to the dry and hot weather in the region. However, together with the production growth, consumption volumes are decreasing by 2 million tons compared to last year, to the level of 116 million tons. Meanwhile, wheat reserves are estimated at 130 million tons, although Chinese statistics are not always reliable.

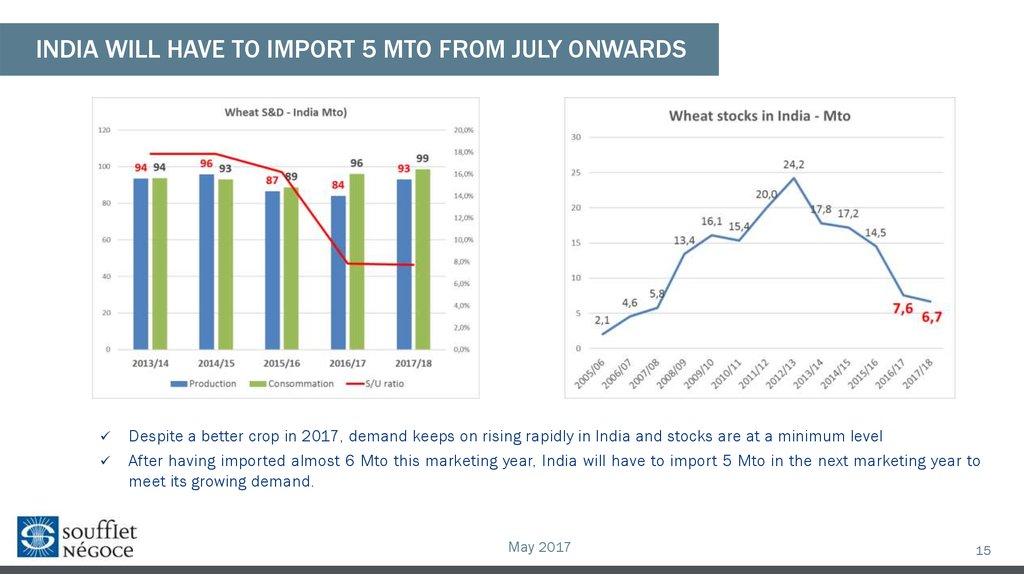

The continuing consumption increase in India, which this year will reach 99 million tons with its own production at 93 million tons, can be considered a positive fact for Ukraine. Given that Indian reserves are at a minimum level, the country will import at least 5 million tons in the season of 2017-2018.

Bull and Bear factors

Record world reserves, good crop prospects in the Black Sea region, expansion of acreage in Argentina and quite low grain sales volumes for the current period by farmers in the EU and the Black Sea region are the factors that cause price reduction. The current trade volume is 2 million tons lower than last year.

The price reduction will be affected by the decrease of wheat reserves in the main exporting countries by about one million tons, which will encourage price strengthening. Besides, lower yields are expected in the US, Australia and Russia. The prices will be supported by the growing demand in India and the activity of the farmers themselves, who can maneuver stocks and refrain from selling grain at low prices due to the constant growth of storage capacities .

At the same time, the exchange fluctuations of the currencies of the main grain producers against US Dollar will have a significant effect on the dynamics of the volumes entering the market.

The AgroExpedition Wheat 2017 team will soon be able to check these forecasts directly in the fields. To be continued.