Back to 2020/21: Is Ukraine’s Wheat Market Experiencing a Déjà Vu?

Photo by: Latifundist.com

The season has only just begun, yet Ukraine’s wheat market is already showing signs that mirror 2020/21: lower yields, higher protein content, a shortage of feed wheat, and a narrowing spread between classes. At first glance, it all points to a familiar scenario. But is 2025/26 really a return to the conditions of five years ago? And if so, what lies ahead?

Weather: a common denominator

Just like in 2020/21, the new crop season began with a lack of moisture in the fall, a warm winter, and a stressful spring — especially in southern regions, where crops lost a significant share of their potential. Even the June rains failed to improve the situation.

Still, weather conditions across the country were uneven. Central and western regions have been showing noticeably better crop conditions, raising hopes that they could partially offset the losses in the south. However, the most recent field reports show that some wheat in western regions being affected by grain smut, a fungal disease triggered by recent rains. These fields require immediate harvesting to prevent the spread of the disease, which could render the grain unsuitable even for feed use.

Milling wheat back in the spotlight

At the start of the 2025/26 season, milling wheat is once again dominating the market. Feed wheat supply is limited, while farmers are mostly offering wheat with protein content between 11.5% and 12.5%, and in some cases over 13%.

We’ve seen this before: in 2020/21, high-protein wheat made up the bulk of the harvest (nearly 60% of total volume), while feed wheat became a scarce commodity. In contrast to the last three seasons — when the share of milling wheat dropped to 25–37% — the current crop structure may be shifting back toward the protein-heavy model characteristic of 2020/21.

However, it’s too early to draw final conclusions: as of 17 July, only 30% of the area has been harvested. The full picture will emerge after harvest wraps up in the central and western regions, where quality and structure may differ significantly.

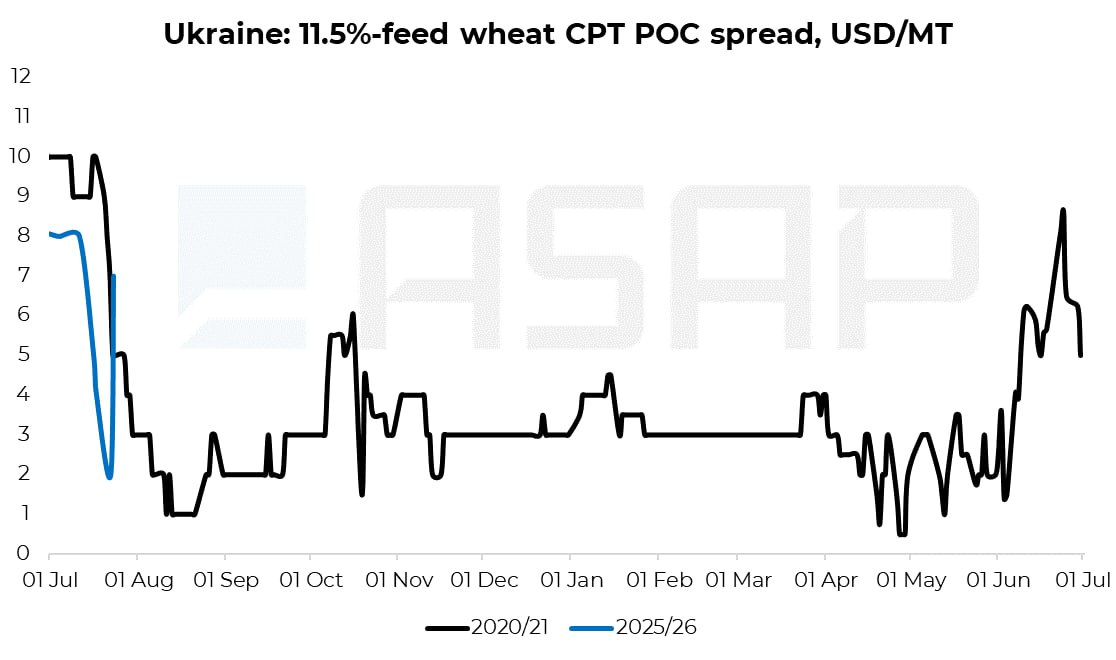

Spread narrows: feed wheat market heats up

One of the clearest indicators at the start of the season is the sharp narrowing of the spread between feed wheat and 11.5% protein wheat. As of 22 Jul, the difference on a CPT basis has dropped to just 2 USD/MT.

The chart clearly shows that the 2025/26 trendline is closely tracking the pattern of 2020/21, when the spread between milling and feed wheat narrowed sharply due to a shortage of feed-quality grain. This year, the market faces the same challenge again: competition for lower-protein lots is intensifying, pushing feed wheat prices sharply higher.

However, as soon as on 23 July the spread between milling and feed wheat has begun to widen, reaching 7 USD/MT on rainy weather in the North and West of Ukraine. On that day, a parcel of 11.5% protein milling wheat was traded at 235 USD/MT CPT POC, while a day earlier, feed wheat was sold at 228 USD/MT CPT POC. Market operators are closely watching how this trend will develop further.

Meanwhile, part of this season’s crop doesn’t fit into traditional classifications — it may have high protein but falls short of milling quality in terms of test weight or gluten strength. If this supply structure continues, elevators and traders may increasingly resort to blending milling and feed wheat to form export lots that meet standard specs, particularly with 11.5% protein. This further blurs the price boundaries between segments and reduces the role of formal classification.

So, current trends in the Ukrainian wheat market have much in common with the 2020/21 season. There’s every reason to believe that 2025/26 may follow a similar path — although this remains only one, albeit a fairly likely, scenario.

Victoria Blazhko, Head of Editorial Content and Analytics at ASAP Agri

| The first results of the current tricky wheat season will be presented by ASAP Agri during the presentation “2025/26 or Just 2020/21 Reloaded? Déjà Vu Grips Black Sea Grain Trade” at the Grain Academy 2025 conference on 30 October in Varna, Bulgaria. Christina Serebriakova, CEO of ASAP Agri and Broker at Atria Brokers, will unpack the story behind the stats — and what it means for the future of Black Sea grain trade. |