Ukraine’s Late-Season Wheat Export Rush Shifts Focus to Egypt, Algeria and Indonesia

Photo by: Latifundist.com

Ukraine’s wheat export structure changed notably in 2025/26, as weak mid-season shipments were followed by an unusually strong export push in the final quarter of the marketing year. The late acceleration was mainly driven by stronger flows to three key destinations — Egypt, Algeria and Indonesia — which together accounted for 62% of total Ukrainian wheat exports. This helped Ukraine reduce ending-stock pressure ahead of the new season.

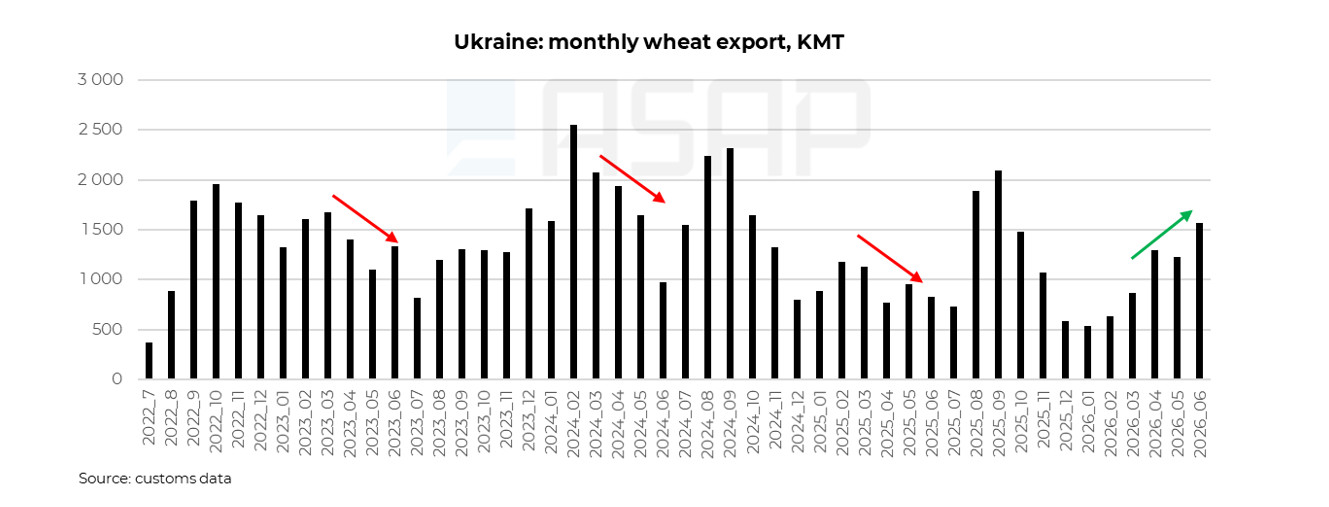

Massive end-season wheat exports

Ukraine exported almost 14 MMT of wheat in 2025/26, including 4 MMT in the last quarter, or 29% of the total volume. This was an unusually high share for the end of the season. For comparison, wheat exports in 2024/25 totalled 15.6 MMT, but only 2.6 MMT, or 16%, were shipped in the final quarter.

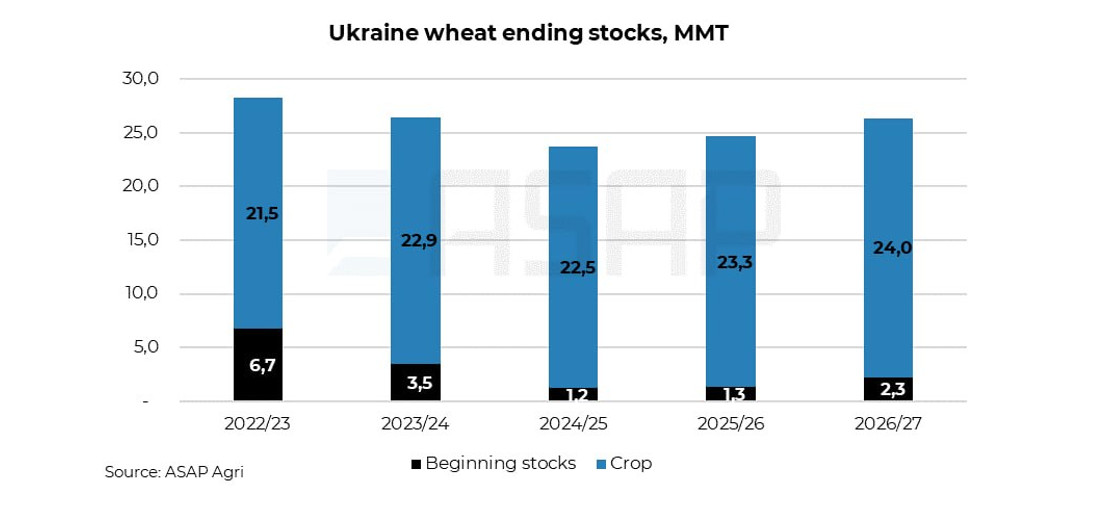

The strong late-season export pace helped Ukraine ease the burden of carry-over stocks. ASAP Agri estimates Ukraine’s wheat ending stocks at 2.3 MMT in 2025/26, while earlier expectations had been higher due to weak export performance in the middle of the season.

However, stocks are still around 1 MMT above the previous year’s level, adding pressure on prices at the start of the new season.

TOP-3 destinations of Ukrainian wheat

With the return of import quotas on Ukrainian grain in the EU, shipments to the bloc declined in 2025/26. Spain, which was the largest destination for Ukrainian wheat in 2024/25 with 3.3 MMT, dropped to fifth place in the ranking in 2025/26, with imports falling to less than 0.7 MMT.

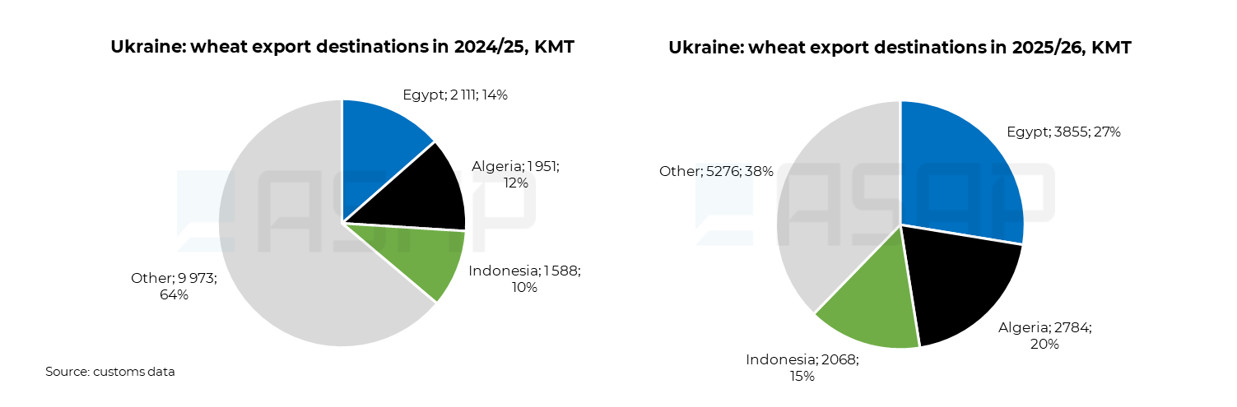

Obstacles in the European market forced Ukrainian sellers to shift more actively toward other traditional destinations, mainly in North Africa and Asia. As a result, shipments increased primarily to Egypt, Algeria and Indonesia.

Egypt’s share of total Ukrainian wheat exports rose from 14% in 2024/25 to 27% in 2025/26. Algeria’s share increased from 12% to 20%, while Indonesia’s share grew from 10% to 15%. Together, these three countries accounted for 62% of Ukraine’s total wheat exports in 2025/26, up sharply from 36% a year earlier.

Improved price competitiveness supported Ukraine in Indonesia later in the season

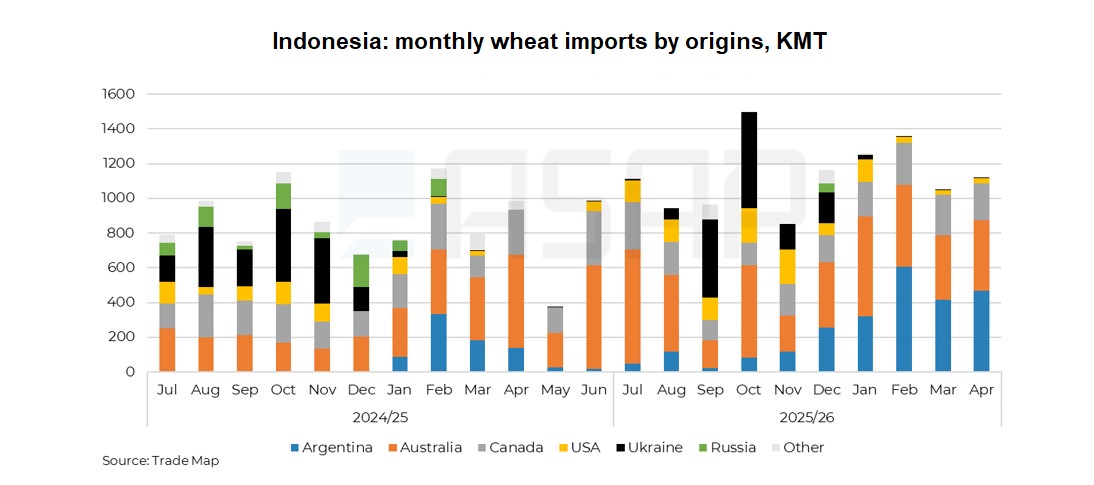

Ukraine strengthened its position in the Indonesian wheat market in 2025/26, supported by improved price competitiveness against rival origins later in the season. Ukrainian wheat exports to Indonesia reached 2.1 MMT, up from 1.6 MMT in 2024/25.

Argentina remained an attractive supplier for much of the 2025/26 season and managed to expand its presence in Indonesia. However, Argentinian wheat prices started to rise in April–May 2026, gradually weakening its competitiveness.

U.S. wheat also became more expensive later in the season. It was highly competitive in 2024/25 and at the beginning of 2025/26, but rising prices reduced some of its price advantage. Still, strong quality characteristics, including a good falling number, helped U.S. wheat maintain its position in the Indonesian market. Additional support came from the U.S.–Indonesia agreement finalized in February 2026, under which Indonesia will facilitate imports of at least 2 MMT of U.S.-origin wheat annually over five years. However, some traders believe Indonesia’s actual U.S. wheat purchases in 2026 could be closer to 1.3 MMT.

Australian wheat also followed an upward price trend in spring 2026. Nevertheless, Australia retained its position in the Indonesian market thanks to logistical advantages and well-established trade flows.

Russia’s presence in Indonesia, meanwhile, virtually disappeared after the country paused imports of Russian wheat in January 2025 due to phytosanitary issues. Indonesia’s Quarantine Agency agreed in August to extend safety certificates for Russian grains, and Russia resumed shipments to Indonesia in October. However, no major follow-up purchases of Russian wheat have materialized so far.

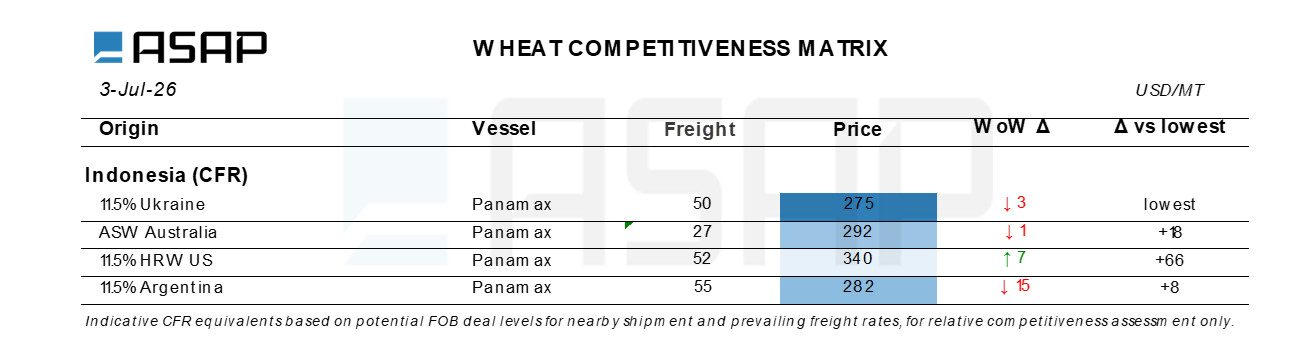

ASAP Agri competitiveness matrix, which is available for Premium subscribers on a weekly basis, shows that as of now, the price of Ukrainian 11.5 protein wheat is also competitive, although some buyers continue to show buying ideas below 270 USD/MT CIF Indonesia for July-August shipment.

Strong North African demand supported Ukrainian wheat export

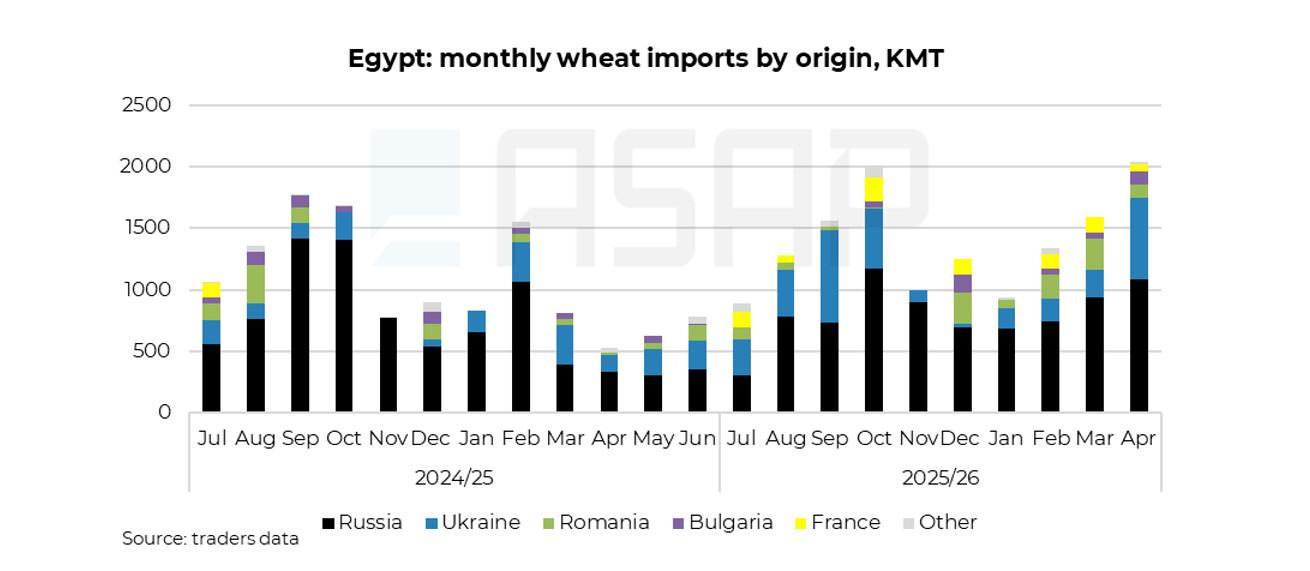

Egypt remained one of the key drivers of Ukraine’s late-season wheat export push. Despite strong competition from Russian origin, Ukraine managed to substantially increase supplies to the Egyptian market in 2025/26. Exports reached a massive 3.9 MMT, up from 2.1 MMT in 2024/25.

The increase was mainly driven by stronger Egyptian import demand, supported by a shift from Russian origin to Ukrainian (as Russia had more high-protein wheat in 2025/26), higher domestic consumption and lower opening stocks in 2025/26, which kept buyers active throughout the season.

Ukraine also continued to strengthen its position in Algeria. Wheat exports to the country rose to 2.8 MMT in 2025/26, compared with 2.0 MMT a year earlier.

In addition to growing domestic consumption in Algeria, Ukraine benefited from the sharply reduced presence of Russian wheat in this market. Russia had been a major supplier to Algeria in 2023/24 and 2024/25, but its share declined in 2025/26. This was partly due to tighter availability of suitable 11.5% protein wheat, stronger competition from Romanian and Bulgarian origins, and a more diversified purchase strategy by OAIC.

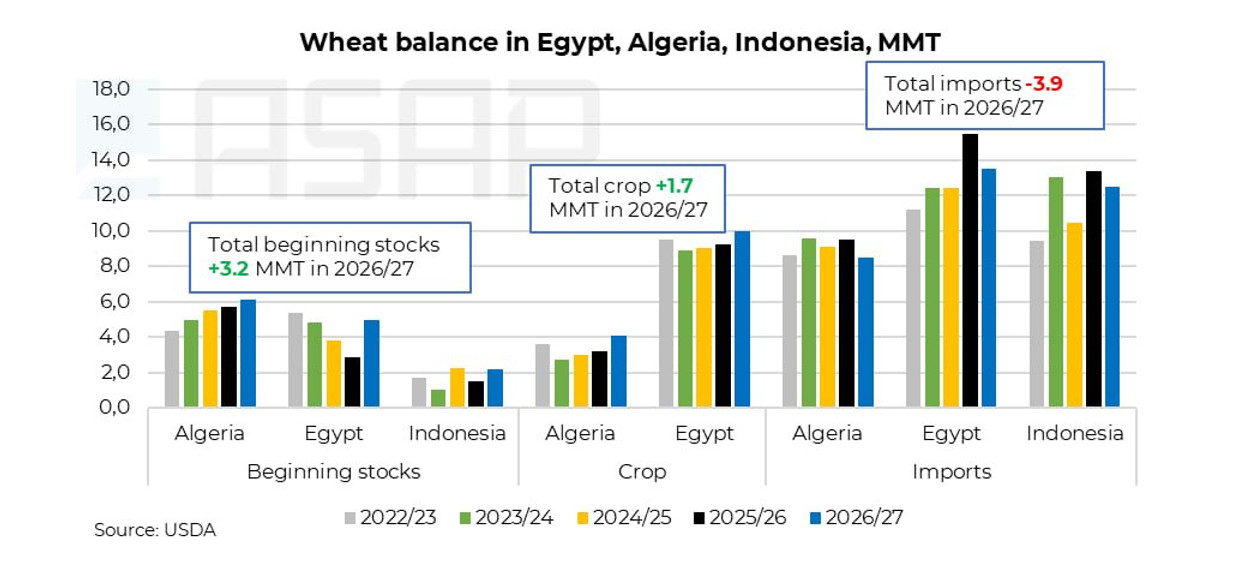

Prospects for 2026/27: lower demand from top buyers may test Ukraine’s export strategy

The 2026/27 season may be more challenging for Ukrainian wheat exports to Egypt, Algeria and Indonesia. Higher opening stocks in all three countries, together with stronger domestic wheat production in Egypt and Algeria, may limit their import needs. The USDA expects wheat imports by all three buyers to decline year-on-year in 2026/27.

Egypt has already become much less active in the wheat market in June, following large recent import purchases and strong domestic wheat procurement. As a result, Ukrainian wheat exports to Egypt may stay limited at the beginning of the 2026/27 season.

At the same time, buyers from Indonesia and Algeria remain present in the market and continue to show buying interest for now.

The key issue for the new season will be competition from other origins. Current forecasts point to a sizable decline in wheat production outside the Black Sea region, which should only be partly offset by larger carry-over stocks among major exporters. However, Black Sea supply is expected to remain ample. Aggressive price offers from Russia already confirm that it is likely to remain a strong competitor for Ukraine, especially in Egypt.

Inna Stepanenko, Senior Grain Market Analyst at ASAP Agri