EU market offers little room for Ukrainian wheat in 2025/26 — ASAP Agri

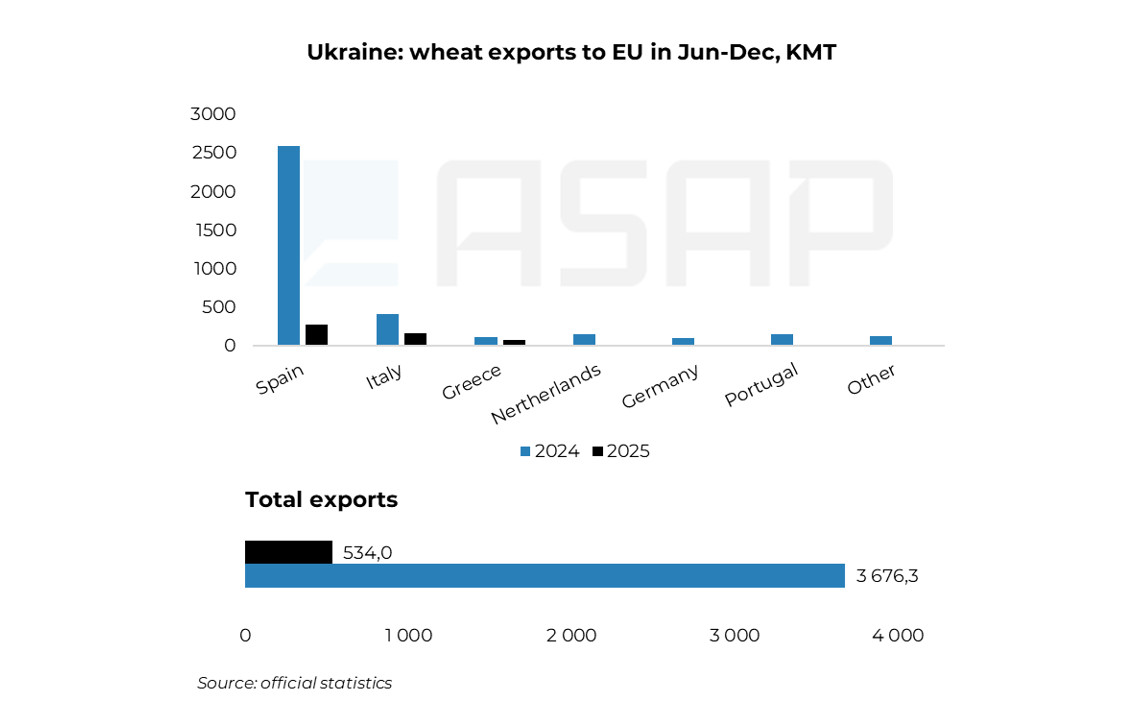

Ukraine failed to fully utilize its EU wheat import quota in 2025, which was set at 758.3 KMT. According to the European Commission, 232.5 KMT of the quota remained unused, which aligns with Ukrainian statistics: Ukraine exported about 534 KMT of wheat to the EU in June–December 2025, says Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri.

The quota was reinstated on 6 June 2025 at 583.3 KMT for the remainder of the year, and in late October, it was increased to 758.3 KMT following a revision of the annual ceiling from 1 MMT to 1.3 MMT. Shipments exceeding the quota are subject to the full EU import duty on soft wheat, estimated at around 95 EUR/MT, effectively rendering such exports economically uncompetitive.

A comparison of data for June–December 2024 and 2025 shows a sharp decline in Ukrainian wheat shipments to almost all EU destinations. The most significant drops were recorded in Spain, where imports fell from nearly 2.6 MMT to about 275 KMT, and in Italy, from 415 KMT to 170 KMT. Shipments to other EU countries in the second half of 2025 remained limited and largely episodic.

Historical data clearly indicate that Ukrainian wheat exports to the EU have been directly determined by the level of the tariff quota. In 2016–2020, when the annual quota stood at around 1 MMT, actual imports from Ukraine hovered close to that level. In 2022–2024, when quota restrictions were lifted, imports increased to 3–6 MMT per year. The reintroduction of the quota in 2025 once again imposed tight constraints on annual export volumes.

At the same time, 2025 proved to be an exception even within this framework: exports to the EU were not only constrained by the quota but also failed to fully utilize the available volume, indicating that additional limiting factors were at play beyond tariff restrictions.

In the second half of 2025, imports of Ukrainian wheat into the EU were further restrained by high internal supply within the bloc itself. According to European Commission estimates, EU soft wheat usable production in 2025 reached 134.4 MMT, the second-highest level on record. Under such conditions, the EU’s need for imports declined significantly, even with quota access available.

“This season, EU demand is largely covered by wheat of French and Baltic origin. Due to declining export competitiveness in third-country markets, EU wheat is being redirected to the internal market. Under these conditions, Ukraine’s 2026 quota (1.3 MMT — ed.) will most likely be utilized mainly for the 2026/27 crop,” said Manuel Alcaraz, General Manager of Cereales y Harinas Garsan, S.L., one of Spain’s leading companies in the marketing of grains, flour, and oilseeds, in an exclusive comment to ASAP Agri.

Against this backdrop, opportunities for Ukrainian wheat on the EU market in the 2025/26 MY remain very limited. This means that in the second half of the season, Ukraine will need to strengthen its presence in alternative markets, primarily North Africa, where demand remains stable. At the same time, competition from russian wheat will remain strong, given russia’s high grain export quota of 20 MMT, set for the period from 15 February to 30 June 2026.