The Corn in the Focus: the USDA June Report Highlights

Over the past few weeks, the market has been looking forward to the new USDA report. Many Ukrainian market participants were worried about the delayed planting progress in the US no less than about own harvesting campaign. The Ukrainian agriproducers could not make their mind whether to trade forward their corn or to hold it till the best prices form. Latifundist.com has selected the key points from the USDA June report.

Corn

Unprecedented planting delays observed through early June are expected to prevent some plantings and reduce yield prospects. As a result, the production forecast for the US in 2019/20 was revised to 347.49 million tons vs. 381.78 million tons in May.

A 34.29 million tons difference, according to Agritel analysts, confirms the assumption of a 3 million acres corn acreage decrease (1.2 million hectares) to 89.8 million acres (36.3 million hectares) and a yield drop to 166 bushels per acre. Thus, the USDA has reduced the forecast of ending stocks in the new campaign to 42.26 million tons, which contrasts with the heavy balance of 2018/19 with reserves above 55.7 million tons.

Beginning stocks are up reflecting a 100-million-bushel decline (4.32 million tons) in projected exports for 2018/19 to 2.2 billion bushels (95.14 million tons), based on current outstanding sales and reduced U.S. price competitiveness.

Corn production for 2019/20 is forecast to decline 1.4 billion bushels (60.5 million tons) to 13.7 billion (592.5 million tons), which if realized would be the lowest since 2015/16.

AgriCensus analysts, following the forecast of a 9% drop in corn production, have noted an increase in corn futures.

"By 13:00 Eastern time, July corn futures were USD 0.13/bu higher at USD 4.30/bu, with September at USD 4.38/bu. Overnight crop progress data initially dampened the enthusiasm around US corn plantings, with progress at the upper end of analysts’ expectations as farmers mustered a significant 16 percentage point increase week-on-week, taking planting to 83% complete," says the message.

The quality of the crop also surprised analysts, as good and excellent ratings came in at 59%, versus expectations of 55%.

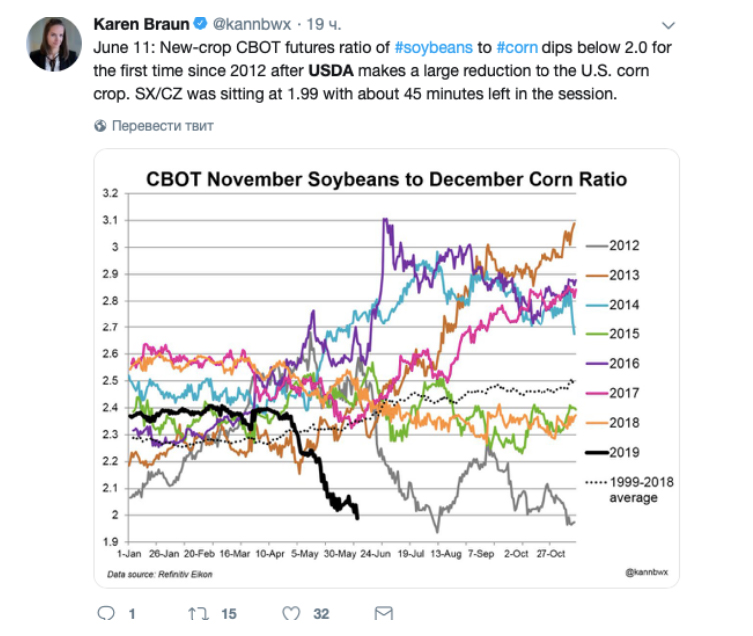

Commenting on the USDA report, Karen Braun, Global Agriculture Columnist at Thomson Reuters, said that the corn/soybean futures price ratio was about 2 (soybean/corn futures price ratio — ed.) based on futures contracts. This situation is observed for the first time since 2012 after a major reduction in the United States.

At the same time, Head of Data & Analytics at MarcoPolo Commodities at Marcopolo Commodities, Elena Neroba, notes that during the last exchange session this ratio was standing at the level of 1.99 for 45 minutes.

Wheat

Production in Russia and Ukraine are each raised 1.0 million tons reflecting favourable weather to date. Projected 2019/20 global trade is expanded 0.8 million tons with a 1.0-million-ton increase for Russia and a 0.5-million ton increase for Ukraine, both due to larger crops. Russian exports are now projected at 37.0 million tons and Ukraine exports are projected at a record 19.5 million.

Partly offsetting is a 0.5-million-ton decrease for EU exports with greater competition from Black Sea origins.

U.S. 2019/20 wheat supplies are down with lower beginning stocks partly offset by slightly higher production. Beginning stocks are down 25 million bushels (1.081 million tons) on increased 2018/19 exports.

Winter wheat production is forecast up 6 million bushels (259.5 thousand tons) to 1,274 million (55.097 million tons) with an increase to Hard Red Winter more than offsetting decreases for Soft Red Winter and White Winter.

Total wheat production is now forecast at 1,903 million bushels (47.27 million tons), up 5.8 million (250.84 thousand tons) bushels from the May forecast.

Exports for 2019/20 are unchanged at 900 million bushels (38.92 million tons) but feed and residual use is raised 50 million bushels (2.16 million tons) to 140 million (6.05 million tons) on reduced projected corn supplies.

Oilseeds

This month’s U.S. soybean supply and use projections for 2019/20 include higher beginning and ending stocks.

Beginning stocks are raised reflecting a 75-million bushel (3.23 million tons) reduction in projected exports for 2018/19 based on lower-than-expected shipments in May and a lower import forecast for China. Although adverse weather has significantly slowed soybean planting progress this year, area and production forecasts are unchanged with several weeks remaining in the planting season.

At the same time, USDA experts lowered the forecast for soybean production in the US in 2019/20 to 112.95 million tons, 8.7% (10.71 million tons) lower from the bulk yield in 2018/19 (123.66 million tons).

They also project a reduction in 2019/20 soybean harvest in the second largest world producer, Argentina, to 53 million tons, 5.4% less than the bulk yield in 2018/19 (56 million tons), yet it is 28.7% more from 2017/18 (37.8 million tons).

Other changes for 2018/19 include increased soybean meal imports and exports, reduced soybean oil used for biodiesel production, and higher soybean oil ending stocks.

The 2019/20 season-average price for soybeans is forecast at USD 8.25 per bushel, up 15 cents reflecting the impact of higher corn prices. Soybean meal prices are forecast at USD 295 per short ton, up 5 dollars. The soybean oil price forecast is unchanged at 29.5 cents per pound.

The 2019/20 global soybean supply and use projections include lower production and stocks compared to last month. Global production is down 0.3 million tons to 355.4 million due to lower crops for Ukraine and Zambia.