Corn could play back its role of market driver — ASAP Agri

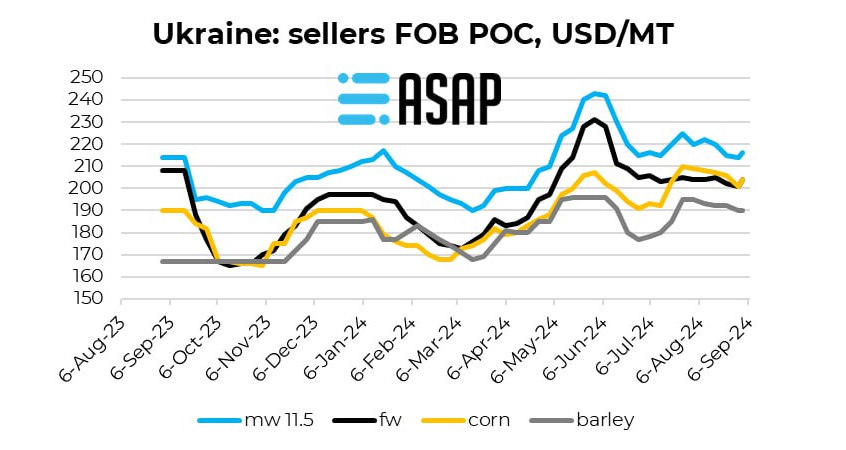

The first cuts of corn in Ukraine have marked the beginning new campaign. At the same time, ASAP Analysts have observed the overtaking of corn prices over feed wheat ones, at least on FOB basis. Corn is then tacking back its role of driver amongst the grain sector.

The 2024 Ukrainian corn production is promised to be in significant reduction compared to last year, by -21% from 29,6 to 23.4 million tons (UGA)/ 24.2 million tons (ASAP Agri). In this context, prospects for export are reduced to a larger extent by almost -30% from 26 million tons last year to 18.5 million tons (UGA)/ 20 million tons (ASAP Agri).

In this context, corn prices have strengthened compared to other grains all along the second half of the vegetative period. Indeed, in the middle of June 2024, Ukrainian corn was discounted by more -20$ vs feed wheat but now is almost at parity with it. The milling wheat premium vs corn is currently only displayed at +10USD, which should prevent 11.5% wheat from price decrease on the local market.

This new market fact can be positive for Ukrainian producers. First of all, at the global level, Chicago corn prices have just recovered above the psychological level of 4$/bu, which should now act as a strong support for the market. In the short-term, prospects for potential cuts in US corn yields should support the market. Note that this may appear on the occasion of the release of the monthly WASDE report. In addition, analysts note that the grain complex is profiting from the support of the oilseeds sector as proven by the Soybean/corn ratio on CBOT and Rapeseed/wheat ratio on Euronext that continue to demonstrate strong value. Dryness in Brazil currently hampering soybean plantings should continue to play in favour of prolongated firmness of oilseeds vs grains.

At this stage, the only downside for Ukrainian corn is that it is relatively expensive compared to the market benchmark, Chicago. The Ukrainian CPT is currently trading at 20 USD above the December maturity, which is quite similar to the situation the market had before the beginning of the full-scale invasion. Since then, it should be kept in mind that operation fees at port have increased because of inherent risks, but a +20USD basis is tenable in local ports especially in the context of farmers retention and appetite of buyers to be renewed soon.