North Africa becomes “heart” of Ukraine’s wheat exports in early 2025/26 — ASAP Agri

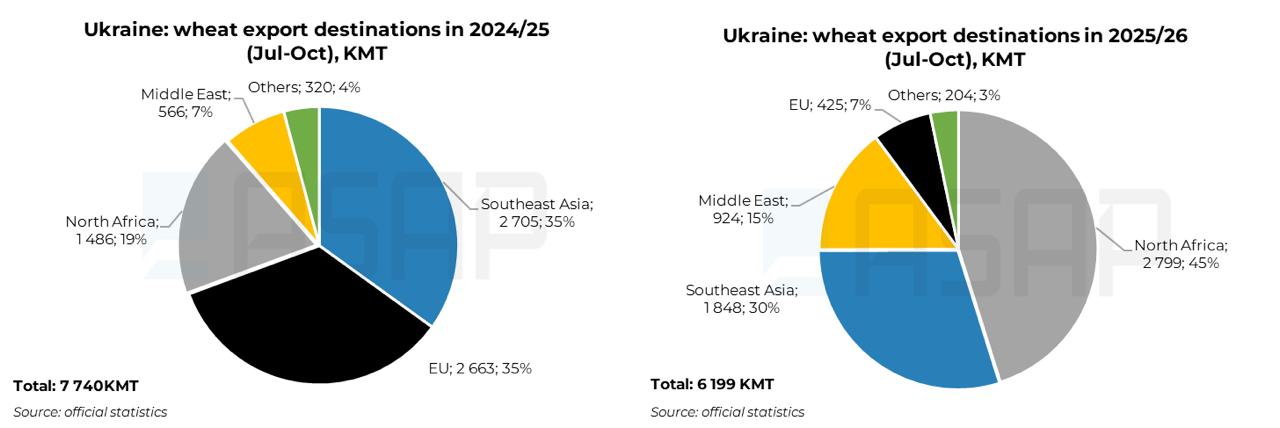

Ukraine’s wheat exports have changed direction this season — literally. The compass that once pointed west now turns firmly south: North Africa has become the main destination, taking almost half of Ukraine’s total wheat shipments between July and October 2025/26, marks Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri.

The numbers speak volumes. A year ago, North Africa accounted for less than one-fifth of exports. Now it commands 45%, fueled by Egypt’s expanding purchases and Algeria’s rising appetite for Ukrainian grain.

Egypt at full sail

Egypt has long been a steady buyer of Ukrainian wheat, and at the start of this season it has clearly tightened its grip on the top spot. Ukrainian vessels once again actively line the berths of Alexandria: 1.84 MMT of wheat have already been shipped in July-October, nearly triple last year’s volume over the same time and not far from the total 2024/25 exports of 2.1 MMT.

For comparison, Spain — last season’s top buyer — imported almost the same volume in 2024/25. This year, Spain’s share collapsed by 85%, leaving Egypt not just as the largest client but as the new center of gravity for Ukraine’s export map.

Algeria joins the fast lane

Right behind Egypt in North Africa comes Algeria, which received 739 KMT of Ukrainian wheat in the first four months of the season — the highest volume ever recorded in trade between the two countries for this period.

If the current pace continues, Ukraine’s wheat exports to Algeria in 2025/26 could surpass last year’s record of 1.95 MMT.

Middle East: a rising bridge

The Middle East has become Ukraine’s third-largest wheat destination, significantly strengthening its position this season. The region’s share climbed to 15%, with total shipments up by more than 60% y/y, reaching nearly 1 MMT in July–October 2025/26.

Yemen remains the largest buyer, with 361 KMT of Ukrainian wheat shipped to the country so far — up 32% y/y. Lebanon also expanded purchases by 35% y/y, reaching 235 KMT, moving closer to last year’s total of 372 KMT and narrowing the gap to its record 579 KMT in 2019/20. Israel followed a similar upward path, with 108 KMT already shipped there — a pace that could bring it close to its all-time peak of 591 KMT in 2015/16.

Meanwhile, Saudi Arabia and Syria have re-emerged as returning destinations. Ukraine had virtually halted wheat exports to Syria after 2016/17, following shipments of 352 KMT in 2015/16, while Saudi Arabia, which once imported 789 KMT of Ukrainian wheat in 2021/22, resumed limited purchases last season. In July–October 2025/26, Syria received 48 KMT and Saudi Arabia 55 KMT, confirming that both markets are cautiously reopening to Ukrainian supply.

Europe’s fade to grey

The European Union, which once absorbed a third of Ukraine’s wheat, has largely stepped off the stage this season. From 2.66 MMT in July–October 2024/25 to barely 425 KMT now — that’s an 84% plunge, driven by the return of EU import quotas, a solid domestic harvest, and stronger competition from nearby origins. The region’s share in Ukraine’s wheat exports collapsed from 35% to just 7%, marking its lowest level in years.

Spain, last year’s heavyweight, slashed imports sixfold to just 276 KMT.

This decline was expected after the EU reinstated import quotas on Ukrainian grain on 6 June 2025. The updated wheat quota, effective 29 October, raised the 2025 limit to 758 KMT (1.3 MMT annually) — up from 583 KMT (1 MMT) under the previous framework.

According to EU customs data, as of 4 November, roughly 292 KMT of the quota remained unused — leaving limited room for additional shipments before year-end. With the annual ceiling in place, exports to the EU in the second half of 2025/26 are also expected to stay subdued, keeping total seasonal volumes well below last year’s 4.7 MMT.

Southeast Asia: battle of the seas

Further east, Southeast Asia’s share in July-October slipped from 35% in 2024 to 30% in 2025.

Despite resilient demand from Indonesia, Vietnam, and Thailand, total volumes fell from 2.7 to 1.85 MMT, as Australia reclaimed market share thanks to competitive pricing and freight.

Still, Indonesia remained Ukraine’s second-largest buyer, although volumes declined by around 13% y/y. The sharpest drop, however, came from Vietnam, where imports fell by more than 35%, reflecting stronger competition from Australian origins.

Overall picture

In total, Ukraine exported around 6.2 MMT of wheat in July–October 2025/26, down from 7.7 MMT a year earlier — a decline of nearly 20%. North Africa and the Middle East now account for over 60% of all shipments, while Europe’s role has shrunk to a quota-bound niche.

Given the EU restrictions, Ukraine will need to redirect around 2–2.5 MMT of wheat by the end of the season. The most promising outlets clearly lie in the MENA region, where demand is largely stable and trending upward, and competition, though fierce, is familiar.

By contrast, Southeast Asia’s growth potential looks limited. Ukraine’s strongest export window to the region is closing, while Australian supply pressure is set to intensify from December onward.

What the new map of Ukrainian wheat exports will look like — and how the Black Sea region is redistributing trade flows — will be one of the central themes at Global Grain Geneva 2025. On 12 November, Christina Serebriakova, CEO of ASAP Agri and broker at Atria Brokers, will moderate the panel “From Wheat to Feed: Black Sea Tender 2025/26”, bringing together leading exporters and buyers for an open discussion on the new challenges, directions, and opportunities of the season.