Futures structure flips: 2026 wheat trades above old crop — ASAP Agri

The record wheat season is not over yet, but the market is already thinking ahead — and pricing the next year higher. The 2026 crop has gained a premium over the 2025 crop, a structure that looks unusual from a seasonal perspective, marks Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri.

As of mid-February, the September 2026 contract on Euronext is trading about 4 EUR/MT above the May contract, while on CBOT, the July contract holds roughly a 3 USD/MT premium over May. Formally, this is classic contango, where deferred contracts trade above nearby ones.

Victoria Blazhko

Head of Editorial Content and Analytics at ASAP Agri

"Yet for a new crop, such a structure is more the exception than the rule. Typically, the old crop gains a premium toward the end of the marketing year as physical supply tightens, while the new crop trades at a discount as future volume."

The current premium, therefore, represents more than a technical signal. The market is already looking beyond the record 2025/26 season and starting to price risks for 2026/27 — lower production and a thinner buffer among key exporters.

From record surplus to a narrowing buffer

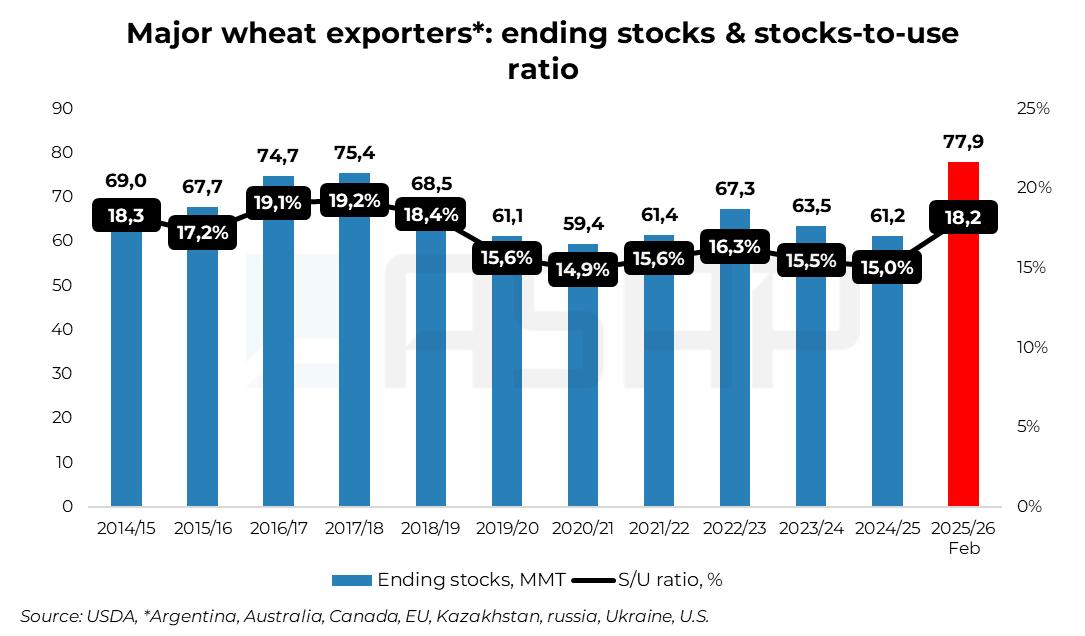

The 2025/26 season remains exceptionally comfortable for wheat markets. Global production has reached a record 842 MMT, carryover stocks are high, and the stocks-to-use ratio among major exporters — the U.S., Canada, Australia, Argentina, the EU, russia, Ukraine, and Kazakhstan — stands near 18%.

These countries shape global export availability, and current stock levels provide a meaningful buffer, explaining why the old crop has not gained a premium: the physical market does not feel tight.

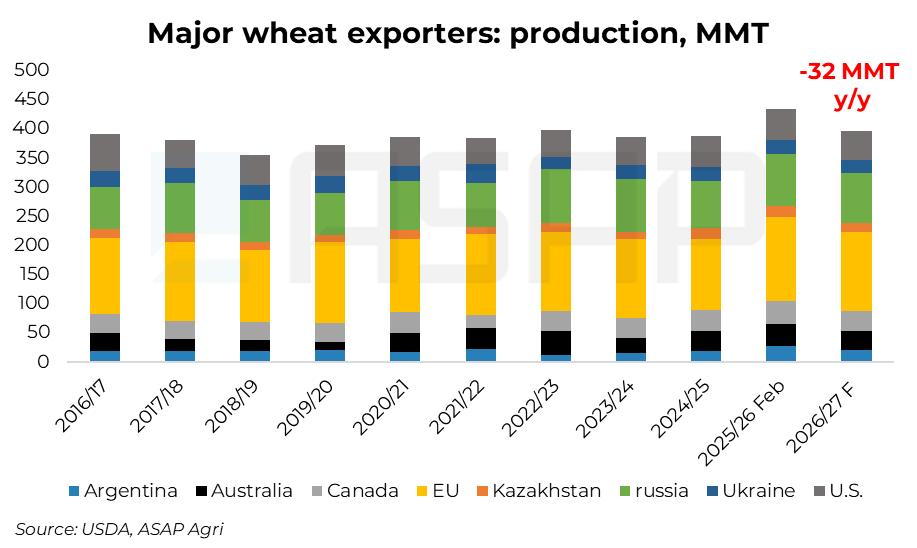

However, forward expectations are less relaxed. Early projections for 2026/27 signal a 7–8% decline in production among the eight major exporters, equivalent to roughly 32 MMT.

Country signals appear broadly aligned. russia may ease from around 90 MMT to 86–87 MMT as yields normalize and acreage declines, while Ukraine’s early outlook stands near 23.

Canada could retreat from a record 40 MMT to 35 MMT, while U.S. output may fall to 50–52 MMT amid multi-year-low winter wheat acreage and persistent drought risks in the Southern Plains.

In the EU, production may decline from about 144 MMT to 135–138 MMT as yields normalize and profitability remains weak. Argentina is expected to produce 21–23 MMT, Australia may return toward 32 MMT, and Kazakhstan could decline from roughly 19 MMT to 15 MMT.

Collectively, this does not create a deficit scenario but does change market tone. If exporters operated with a comfortable buffer in 2025/26, that cushion may narrow noticeably in 2026/27.

It is this adjustment — about 32 MMT across key exporters — that the futures curve is beginning to reflect. Still, these are early estimates that will be revised, and weather could amplify the production decline.