Turkey chooses russian sunflower meal over Ukrainian product — ASAP Agri

Markets do not change overnight — they shift gradually, until at some point the numbers begin to reflect a new reality. That is precisely what has happened in Turkey’s sunflower meal import market, which a decade ago was defined by balanced competition between Ukraine and russia but has since evolved into a near-single-supplier structure, says Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri.

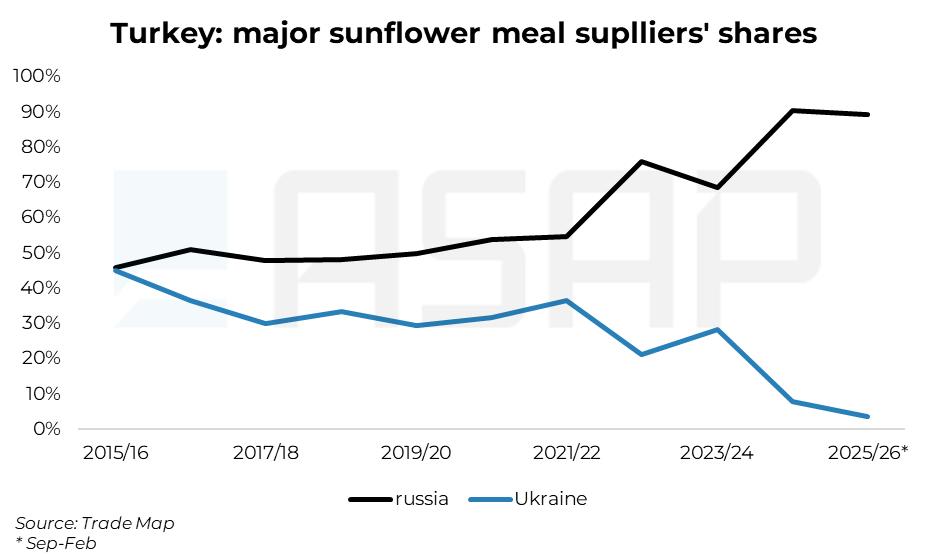

In 2015/16, Turkey’s sunflower meal imports were almost evenly split, with Ukraine and russia each accounting for around 45%. Over the following years, this balance began to tilt: by 2021/22, Ukraine’s share had declined to roughly 30%, while russia had expanded to about 50%.

After 2022, the shift accelerated sharply. In 2022/23, russia’s share rose to around 75%, while Ukraine’s fell to 20%. The change was not only about volumes, but also about risk perception. Lower crushing activity, disrupted logistics, and unstable supply made Ukrainian meal less predictable for a market that depends on consistent, large-scale procurement. At that point, russia did not simply fill the gap — it came to be perceived as the more reliable supplier.

Even after a partial recovery in Ukraine’s position in 2023/24, lost ground was not regained. By 2024/25, russia’s presence had climbed to around 90%, while Ukraine’s dropped to just 8%. In the current season (September 2025 – February 2026), the imbalance has become even more pronounced: russia continues to account for roughly 90% of imports, while Ukraine’s contribution has declined to about 4%.

The main driver of this trend was the shift in EU trade policy. As of 1 July 2024, the European Union introduced a safeguard duty of 95 EUR/MT on imports of sunflower meal from russia and Belarus, significantly limiting russian access to the European market. As a result, part of these export flows was redirected to alternative destinations, most notably Turkey.

Turkey moves out of Ukraine’s focus and becomes a key market for russia

This is clearly reflected in Ukraine’s export flows. Sunflower meal shipments to Turkey, which previously averaged 300–370 KMT annually, have dropped sharply since 2022: to 191 KMT in 2022/23, followed by a brief recovery to 376 KMT in 2023/24, before falling again to 81 KMT in 2024/25. In the current season (September–March 2025/26), exports total just 18 KMT.

The change is equally visible in the export structure. Turkey’s share has declined from a stable 8–10% to just 1%. These volumes have not disappeared but have been redirected. China has emerged as the dominant outlet, with its share rising to around 65% in 2025/26, while the EU — despite a notable decline this season — remains the second core market.

As a result, Ukraine’s export model has shifted toward concentration on China and the EU, while Turkey has effectively dropped out of its key destinations.

At the same time, Turkey has become one of russia’s primary export outlets. According to OleoScope, russia shipped around 1.01 MMT of sunflower meal in the first six months of the 2025/26 season (September–February), of which approximately 312 KMT went to Turkey, making it the largest single destination.

Another factor influencing the market is the divergence in harvests among key Black Sea producers. In the 2025/26 season, russia harvested a substantial sunflower crop (around 17–18 MMT), while in Ukraine, adverse weather conditions led to a significant drop in output to 10.8 MMT, according to ASAP Agri estimates. This has increased the potential supply of sunflower meal from russia, although export pace in the first half of the season was partly constrained by economic factors, including a strong ruble and weak crushing margins.

This imbalance in supply has been reflected in prices.

Price advantage as the decisive factor

In February–March 2026, russian sunflower meal offers on a FOB Black Sea basis were in the range of 215–220 USD/MT, compared with 235–240 USD/MT FOB POC for Ukrainian product. This translates into a stable price gap of around 15–20 USD/MT in favour of russian origin.

At the beginning of April, Ukrainian offers remained broadly unchanged at around 240 USD/MT FOB POC, while russian prices rose to approximately 225 USD/MT. The increase was partly driven by the reinstatement of the export duty on sunflower meal at around 750 RUB /MT (approximately 9–10 USD/MT), as part of the floating “sunflower damper” mechanism introduced in 2022 to regulate export flows in line with market conditions.

The duty is reviewed monthly: it is reduced or set to zero during periods of weaker global prices to support shipments and increased when prices rise to curb exports. This was evident in January–March 2026, when the duty was set at zero, supporting export activity and adding pressure to external markets.

Despite the reintroduction of the duty, the price gap remains significant, and russian sunflower meal continues to be competitive in the Turkish market.

Ultimately, Turkey is choosing primarily the cheaper product, which, in this case, is also supplied by an exporter perceived as more predictable and reliable. In a segment where sunflower meal is largely interchangeable and feed costs are critical, price remains the key driver of demand, while supply reliability reinforces that advantage.