Weather market returns: why new-crop wheat prices rise — ASAP Agri

The Ukrainian wheat market has begun to follow the pricing structure established by Euronext several months ago. While new-crop wheat in Ukraine is not yet consistently trading at a premium to old crop, the spread between the two has effectively disappeared.

As of 7 May, ASAP Agri data showed sellers offering Ukrainian 11.5% protein milling wheat at 240 USD/MT FOB POC for both old and new crop. On a CPT basis, buyers were willing to pay around 224 USD/MT regardless of season, Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri, told Latifundist.com.

Victoria Blazhko

Head of Editorial Content and Analytics at ASAP Agri

"For the Ukrainian market, this marks a major shift compared to last year. In early May 2025, new-crop wheat on a CPT basis was trading at nearly a 20 USD/MT discount to old crop. More broadly, the forward market last season started at much lower levels, largely because buyers were still pricing a significant war-risk premium into Ukrainian grain. This year, that premium has nearly disappeared thanks to the stable operation of Ukraine’s sea export corridor."

Ukraine’s wheat market is now clearly moving in line with the global trend, where prices have continued to strengthen. The main driver is the expectation of a significant decline in global wheat production in the new season. The market has effectively entered a classic “weather market” phase, where any risks to crop development are quickly reflected in prices.

This is exactly the scenario ASAP Agri outlined back in February in an article for Latifundist. At the time, we noted that after the record 2025/26 season, the new-crop futures market was beginning to price in lower wheat production among key exporting countries — a trend that was eventually expected to spill over into the physical market.

Back then, these were only preliminary estimates. ASAP Agri projected that 2026/27 wheat production across eight major exporters — the EU, russia, Ukraine, the US, Canada, Australia, Argentina, and Kazakhstan — could decline by around 32 MMT y/y.

Ahead of the release of the first WASDE report with new-season balances on 12 May, ASAP Agri reviewed the initial forecasts from the USDA Foreign Agricultural Service (FAS USDA) to assess what the market may see in the report.

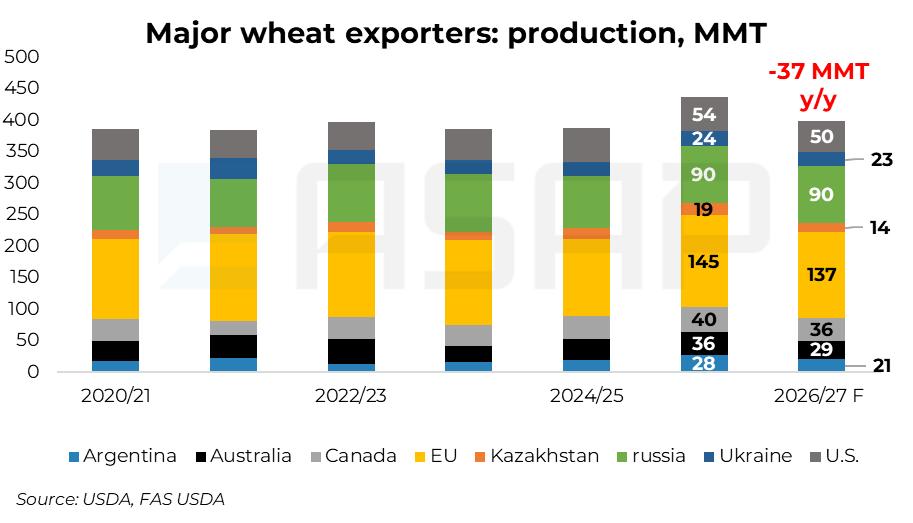

According to current FAS USDA projections, wheat production across the eight key exporters could decline by approximately 37 MMT y/y. In other words, current market expectations broadly confirm the scenario ASAP Agri highlighted several months ago.

The largest production decline is expected in the European Union, where wheat output may fall from more than 145 MMT to 136.8 MMT. After the record 2025/26 season, yields are expected to return closer to historical averages, while planted area is also projected slightly lower.

A significant decline is also expected in Australia and Argentina, both of which harvested record crops in 2025/26. Australian wheat production could fall from around 36 MMT to 29 MMT due to reduced acreage and rising drought risks in the event of an El Niño development. In Argentina, production is forecast to decline from 27.8 MMT to 20.7 MMT as yields normalise following an exceptionally favourable season.

Canada and Kazakhstan, after unusually strong harvests last year, are also expected to cut production by 4–5 MMT to 36.2 MMT and 14 MMT, respectively. According to FAS USDA estimates, the key drivers include yield normalisation, dry weather conditions, and lower fertiliser application amid weaker grain prices.

In the United States, the market is currently looking at wheat production of around 50 MMT, roughly 6% below the previous season. One of the main reasons is a decline in planted area to the lowest level since 1919. In addition, poor winter wheat conditions and yield risks could push final output even lower.

Ukraine and russia currently appear relatively stable compared to other major exporters. FAS USDA estimates Ukraine’s wheat crop at 22.7 MMT, around 5% below last year’s level. In russia, local analysts expect production at around 89.7 MMT versus roughly 90 MMT in the previous season. For both countries, weather conditions and yield potential remain the key risks, particularly following April frosts.

Combined wheat production among the major exporters could decline from 437 MMT to around 399 MMT, which would remain close to the five-year average. At the same time, exportable supply — defined as production plus carry-in stocks minus domestic consumption — is expected to decline much more modestly, by only 10.5 MMT to 255.1 MMT.

"After the record 2025/26 season, the world is entering the new marketing year with comfortable carry-in wheat stocks that partially offset the expected decline in production. As a result, the market appears to be moving back toward a more balanced supply situation rather than into a phase of acute shortage."

That is why the current rally still looks primarily weather-driven. Depending on weather developments and crop conditions across key producing countries, volatility may continue to rise, potentially supporting further gains in wheat prices.

However, once harvesting accelerates across the Northern Hemisphere, global wheat prices — including Ukrainian ones — could once again come under traditional seasonal pressure from incoming new-crop supply and a renewed focus on physical availability.