Ukraine risks missing the last good barley prices — ASAP Agri

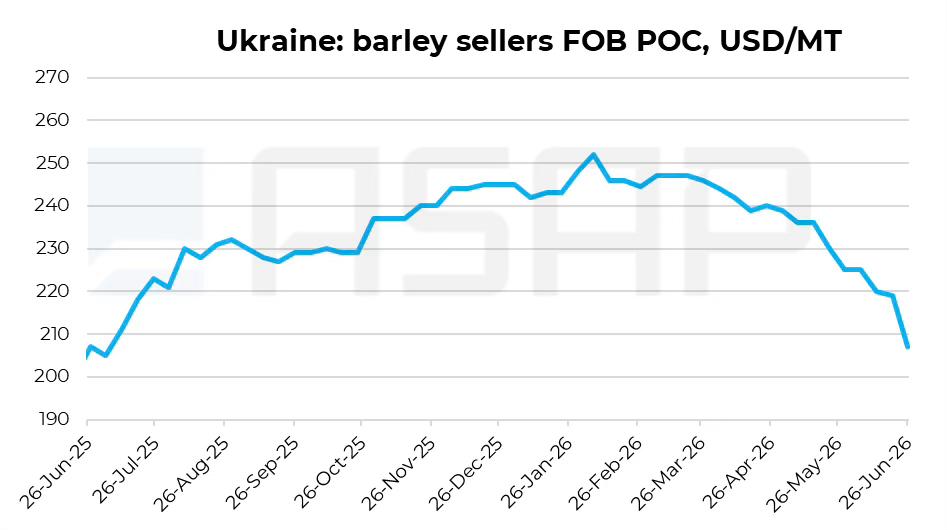

Prices for Ukrainian new-crop barley have finally started to decline more actively. Over the past 10 days, CPT levels have lost around 17 USD/MT. However, the main problem is that this decline appears to have started too late, marks ASAP Agri's Senior Grain Market Analyst Inna Stepanenko.

Ukrainian exporters tried to keep prices at high levels for too long, while Moldova had already been offering barley cheaper for several weeks and was therefore more actively covering demand in the region.

Ukrainian barley is still not competitive enough

In the coaster segment, Ukrainian barley still looks insufficiently competitive.

“At the beginning of July, Ukrainian barley was assessed at around 200 USD/MT FOB Danube, while Moldovan barley was about 10 USD/MT cheaper. That is why most recent deals in the region were mainly done for Moldovan origin,” said Dmitry Kromkin, broker at Atria Brokers.

The situation in the handysize segment also remains difficult. Ukrainian barley declined to around 204 USD/MT FOB at the beginning of July, but it is still more expensive than Russian barley, which is assessed at around 200 USD/MT FOB Novorossiysk.

“At these levels, Ukrainian origin was calculating at around 250 USD/MT CIF Saudi Arabia, while buyers’ interest, according to traders, was closer to 240 USD/MT. This means the Ukrainian price still needs to be lower to compete properly,” said Christina Serebryakova, CEO of ASAP Agri and broker at Atria Brokers.

Buyers are still there, but the window of opportunity is narrowing

Demand for barley is still present, but it is not unlimited. Part of July demand has already been covered with Moldovan barley. According to market participants, Moldovan suppliers have almost sold out their July positions and are already moving to August shipments.

Right now, Ukrainian barley may still have a chance to cover part of the remaining July demand. But for that, prices need to be more realistic.

If Ukrainian sellers wait too long again, buyers may either switch to other origins or lower their price ideas even further.

Ukraine’s harvest started with high yields

Barley harvesting has already started in southern Ukraine. The largest areas have so far been harvested in Mykolaiv region, with smaller areas in Kherson region, while Odesa region is only entering the harvest campaign.

Initial yield results look very strong, at around 4 MT/HA. This is a good start and could push the market to revise crop expectations higher.

If these results are confirmed further, pressure on Ukrainian prices may increase. In this case, Ukrainian barley, especially on the Danube, may be forced to move closer to Moldovan-origin levels.

Competition in the global market is increasing

In France, the harvest started exceptionally early amid scorching June weather. Initial reports point to mixed winter barley yields but good grain quality. Warm and dry weather forecast for the next two weeks could accelerate harvesting further, with the prospect of almost the entire crop being gathered by mid-July.

Russia has also started harvesting. Fieldwork is currently progressing in key southern regions, while initial yields, as in Ukraine, are at a high level and significantly above last year’s figures.

Turkey could become an additional pressure factor, as it may potentially return to the export market in the new season with volumes of around 1 MMT or even more.

“Besides the risk of additional barley volumes from Turkey, competition and price pressure may also intensify due to weaker import demand from the countries that were the main buyers of Turkish barley in 2024/25. This primarily refers to MENA countries. Many of them, including Iran, Iraq, Morocco and Syria, are expected to harvest larger domestic crops in 2026, which will reduce their import needs,” said Salih Karagöz, broker at Atria Brokers.

Overall, many traditional barley importers may have better domestic crops this year than last year. This means there will be less ‘hungry’ demand, while competition for buyers will become tougher.

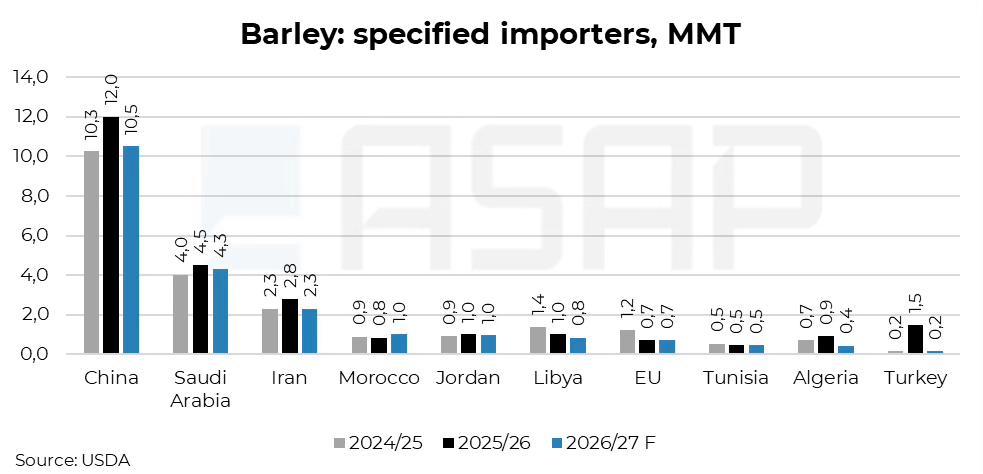

There is also no sign yet of very active demand from China specifically for Ukrainian barley. There are CPT purchases of grain with Chinese specification on the market, which means some volumes have likely already been contracted. However, this is still not enough to talk about strong support for Ukrainian prices.

Spain may also remain an important destination for Ukrainian barley, but demand there is limited by EU import quotas. Therefore, this demand is unlikely to fully solve the sales problem for Ukrainian origin.

Outlook

Ukrainian barley is likely to remain under pressure in the near term. High initial yields in Ukraine, active supply from competitors and weaker demand from key importers give the market little reason to hold high prices.

The main risk for Ukraine now is adapting too slowly to the real level of buyers. If prices do not become competitive quickly, Ukraine may miss the last relatively good sales opportunities at the start of the season.

At the same time, a further decline in Moldovan prices may slow due to logistics problems and a shortage of rail wagons. Market participants also reported restrictions on truck movement because of severe heat in the country, which is currently slowing grain deliveries to ports and could provide short-term price support.

This could create a short window of opportunity for Ukrainian barley. But the market will be able to use it only with more aggressive and realistic pricing.

ASAP Agri premium subscribers will receive the updated Ukrainian barley balance and a forecast of its key sales destinations in the new report format at the beginning of July.