The World Is Entering an Era of Agricultural Surplus. Why This Is a Chance for Ukraine

Photo by: Grain Ukraine Conference

The future of agribusiness is not grain exports. Cesar Soares on Ukraine, China and the world by 2050

If Latifundist.com were a lifestyle outlet, this interview with Cesar Soares would tell you that his wife is Ukrainian and was born in Izium. He would also share how his family rescued his father-in-law and mother-in-law from the occupation. Today, the whole family lives together in Switzerland, his home smells of Ukrainian borshch, and he suspects his wife’s parents of having a secret arrangement with local farmers, buying up all their red beets, cabbage and carrots.

But this interview is about something much bigger.

Soares believes the global agricultural sector is on the edge of fundamental change. Over the past half-century, the main challenge was to produce enough food. In the coming decades, the problem may be very different: a surplus of agricultural products. In that world, says the analyst and founder of CAS Consultancy, the winners will not be those who grow more grain, but those who create new demand for it.

The world will produce more than it consumes. What does this mean for Ukraine?

Latifundist.com: Cesar, you visit Ukraine quite often. After everything the country has been through, what impresses you the most?

Cesar Soares: People’s ability to adapt. That is one of the key things when we talk about the future.

Look at technology. For example, the first version of ChatGPT appeared after the start of Russia’s full-scale invasion — in November 2022. So artificial intelligence in the form we actively use today has existed for a very short time. But it has already become an integral part of our lives.

Four years ago, we had Google. Today, we already think about the future through the lens of AI. This shows how quickly people, businesses and entire industries can change.

Latifundist.com: If we look beyond the challenges of a single season and take the horizon to 2050, what global trend will change agriculture the most?

Cesar Soares: The most underestimated and, at the same time, the least understood trend is that global agricultural production continues to grow.

If you look at the past 20, 25 or even 50 years, global agricultural output has been increasing almost continuously. There have been droughts, poor harvests and periods of tighter supply. But in the long term, we see steady growth in production, yields and productivity across the main crops.

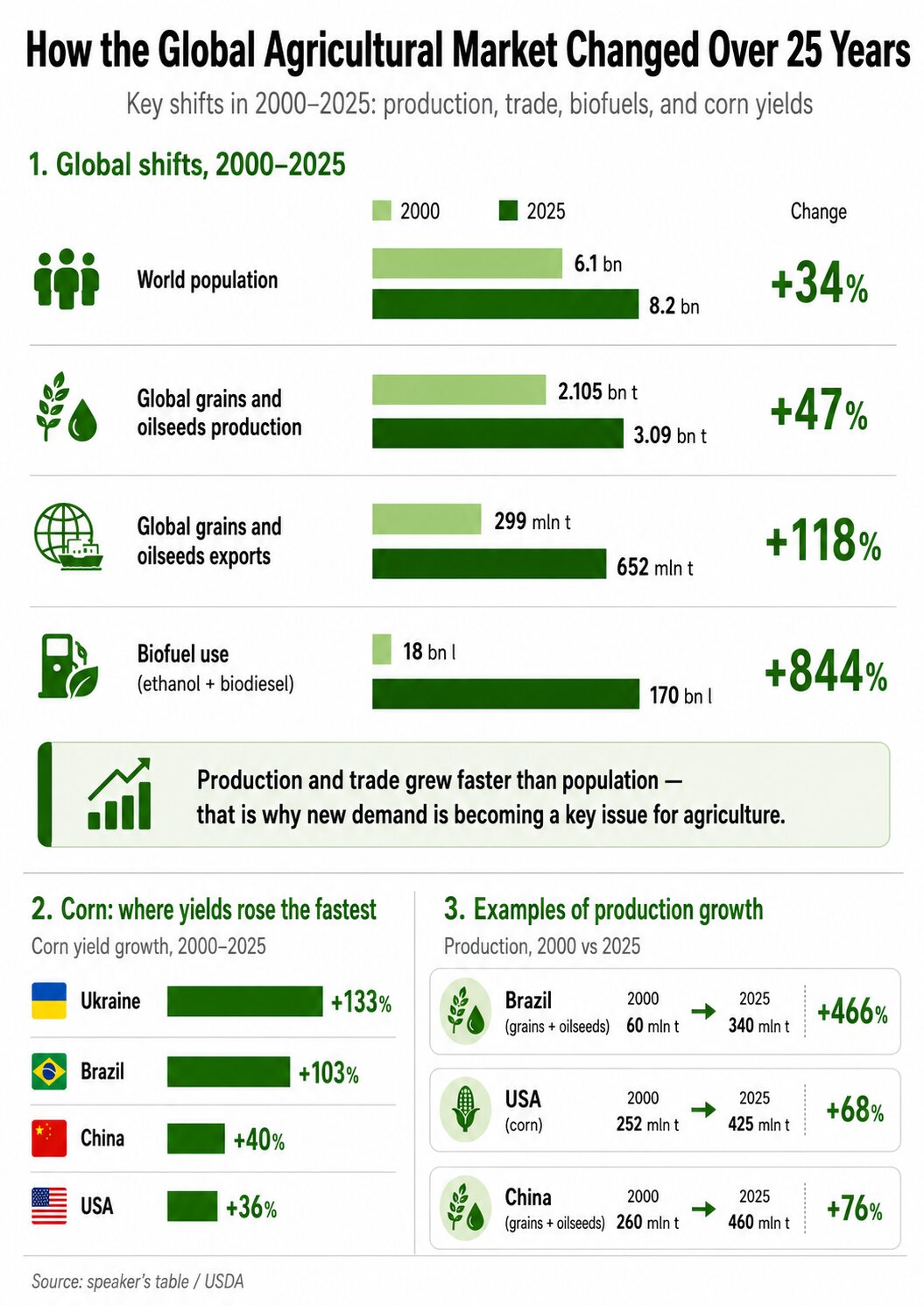

If we narrow the focus to grains and oilseeds, the scale of change is very clear in the numbers. Between 2000 and 2025, the world’s population grew by 34%, while global grains and oilseeds production increased by 47%, reaching 3.09 billion t. Trade grew even faster: combined global exports of grains and oilseeds rose from 299 million t to 652 million t, or by 118%.

Corn is a good example. Today, the average corn yield in Ukraine is roughly 6.5–7.5 t/ha. Twenty years ago, it was around 3–4 t/ha. This shows how quickly technology, genetics and farm management can change what is possible in agriculture.

The trend looks even more striking in dynamics: between 2000 and 2025, corn yields in Ukraine increased by 133%. For comparison, they rose by 103% in Brazil, 36% in the U.S. and 40% in China. So Ukraine still has strong catch-up potential, but part of that potential is already being realized.

Latifundist.com: There are already farms in Ukraine harvesting 11–12 t/ha of corn.

Cesar Soares: Yes. And that is already the level of very efficient production. In the U.S., the average corn yield is above 185 bushels per acre, or around 11.6 t/ha. Ten or twenty years ago, numbers like that seemed almost out of reach.

But it is important to understand the role of technology correctly. Technology does not so much “increase” yields as prevent them from falling. Every plant has genetic potential. But in the real field, that potential is limited by drought, heat, lack of moisture, stress and disease. The job of technology is to minimize losses and bring the result closer to what the plant can theoretically deliver.

It is a bit like marathon runners. People have not fundamentally changed over the past few decades, but results have improved thanks to training, nutrition, analytics and equipment. Agriculture is similar: technology does not change the nature of the plant, but it creates conditions in which the plant can realize more of its potential.

That is why I believe the long-term trend will remain unchanged: global agricultural production will keep growing.

Latifundist.com: But if production keeps growing, will consumption grow at the same pace?

Cesar Soares: This is where we come to a turning point.

For the past 50 years, the world produced more every year. But demand was also growing: the population was increasing, people were consuming more, including more carbohydrates. In some regions, this even led to an obesity crisis.

Now the situation is changing. Global population growth is slowing. In some countries, fertility is already below replacement level. This means demand will no longer grow the way it used to.

At the same time, production efficiency keeps improving. In the past, producing 1 kg of chicken meat required around 3 kg of feed. Today, very efficient producers can get 1 kg of meat from less than 2 kg of feed. In aquaculture, for some fish species, it is possible to produce 1 kg of fish meat from 1 kg of feed.

Latifundist.com: So the world may face not a shortage, but a surplus of agricultural products?

Cesar Soares: Exactly. Demand stabilizes, while production continues to grow. You produce more and more, but consume roughly the same amount. Maybe a little less, maybe the same. And then you get a surplus.

The key question for the future is: what do we do with that surplus?

And this is a major opportunity for Ukraine. If production continues to grow faster than traditional food demand, the world will increasingly face the risk of surplus. Then the key issue will not only be yields, but new channels for using grain. Without them, prices will remain under pressure.

So the future of agriculture is not only about how to grow more. It is about how to create new demand.

Latifundist.com: What exactly is the opportunity for Ukraine here?

Cesar Soares: Ukraine is already a micro-model of this future. It produces far more than it consumes.

Before the war, Ukraine harvested more than 40 million t of corn and exported over 25 million t. The balance has shifted since the war started, but even with a crop of around 30 million t, the country can still export 22–24 million t of corn a year. Among major exporters, this is one of the highest export-to-production ratios.

For a Ukrainian farmer, this means very limited choice. In many countries, a producer has several sales channels: a feed mill, an ethanol plant, food processing, livestock, or a port. He can look at where the price is better.

In Ukraine, the choice for corn and wheat is much narrower. Domestic consumption is low, so the farmer often has to send 70%, 80%, sometimes 90% of production to the port.

And the ports are in the south. A large share of production is in the center, north and west of the country. That means long logistics distances and high costs.

Latifundist.com: What changes if demand is created inside the country?

Cesar Soares: The farmer gets a choice.

Imagine we build plants and create demand in the center of the country. The farmer no longer has to move grain only to the port. He can send it to a plant near Kyiv, near Lviv or in another region. He can sell not only into the export channel, but also into domestic processing.

That raises the price for the farmer. And a higher price stimulates more production.

So for Ukraine, expanding the domestic demand base is one of the most important ways to increase agricultural production.

I sometimes say: why not turn all Ukrainian corn into ethanol? It sounds like a joke, but not entirely. Why not?

People tell me: “What happens to the export sector? It disappears.” No. The farmer will plant more. If there is export demand, domestic demand and demand for a processed product, production will grow.

Global trends show why this topic is becoming more important. Between 2000 and 2025, global biofuel use — ethanol and biodiesel — grew from 18 billion liters to 170 billion liters. That is an increase of 844%. So bioenergy has already become one of the fastest-growing channels for creating new demand for agricultural raw materials.

Ukraine can produce 125 million t of grain. But the key question is what it will do with it

Latifundist.com: At Grain Ukraine 2026, the idea that Ukraine could produce more than 100 million t of grain was mentioned several times. Andriy Stavnitser, in particular, spoke about 125 million t. How realistic is this scenario?

Cesar Soares: I think it is possible. But not within the current model.

If Ukraine tries to increase production only through raw grain exports, it will face tough competition from the U.S. and Brazil. The Brazilian farmer has scale, huge domestic demand and strong infrastructure.

Brazil’s example shows how quickly a country’s agricultural weight can change. Between 2000 and 2025, Brazil’s grains and oilseeds production grew from 60 million t to 340 million t — an increase of 466%. But that growth was not based only on raw commodity exports. It also relied on scale, domestic demand, infrastructure and the development of bioenergy.

So the path to 100–125 million t is not about simply exporting more raw grain. It is about creating domestic demand, developing processing, bioenergy and value-added production.

Ukraine has one of the cheapest grain bases in the world, talented people and a huge surplus of raw materials. This can become the foundation for the next stage of growth.

Ukraine also needs energy. But grains, oilseeds and biomass are energy too. They need to be converted.

So Ukraine does not lack energy components. It lacks the conversion of those components into an energy product.

This is exactly where Ukraine’s competitive advantage lies. Not in simply exporting more grain, but in adding value, creating value and exporting value.

Latifundist.com: You say the next 25 years will be different from the previous ones. Why?

Cesar Soares: In recent decades, the winners were those who built logistics for growing demand. You built ports, railways and roads. You expanded farms, machinery and elevators. You made the system bigger and more efficient. And it worked while the world was consuming more and more grain.

The numbers confirm this: between 2000 and 2025, global grains and oilseeds production increased by 47%, while their combined exports grew by 118%. So global trade was growing much faster than production itself, and logistics really was one of the key assets of the previous model.

In that model, the winner was whoever controlled the supply chain. But if we are moving into a world of surplus, the logic changes.

The winners will not only be those who control the movement of grain. The winners will be those who create new demand.

Latifundist.com: What do you mean by new demand?

Cesar Soares: Imagine that a major share of future demand comes from bioethanol.

Then the most valuable asset will not be a grain export terminal. The most valuable asset will be the infrastructure for producing, transporting and selling ethanol.

The same applies to sustainable aviation fuel, biochemicals, biomaterials and other processed products.

All these sectors also need logistics, investment and supply chains. But these are different value chains.

So the key question for the next 25 years is who will create new demand and who will control the new markets.

Latifundist.com: Which countries have the best chance of benefiting from this transformation?

Cesar Soares: First of all, we need to look at countries with the largest surplus of agricultural production relative to domestic consumption.

And here Ukraine is one of the most interesting examples in the world.

The U.S. consumes around 330 million t of corn domestically every year, while total use, including exports, exceeds 410 million t. It already has a huge domestic-use base: livestock, feed, ethanol and the food industry.

Between 2000 and 2025, U.S. corn production grew from 252 million t to 425 million t, or by 68%. But the key point is not only the volume. A large share of that corn stays inside the country and works in processing, feed, livestock and ethanol. That is why the American farmer has more sales channels than the Ukrainian farmer.

Ukraine has a completely different structure. Almost every Ukrainian farmer effectively builds port logistics into their price. So any alternative to exports automatically creates additional value.

If you can give the farmer cheaper logistics and one more buyer, the farmer will reward you with higher production.

Latifundist.com: So Ukraine’s main reserve is not only yields, but also domestic demand?

Cesar Soares: Exactly. Ukraine still has room to increase yields. But an even bigger reserve is creating new uses for agricultural raw materials.

We often talk about exports. But the future may not be about exporting more corn or wheat.

The future may be about exporting ethanol, food products, bioenergy, biochemical products, feed and animal protein.

Latifundist.com: How important will Ukraine’s integration into the EU be in this process?

Cesar Soares: Once Ukraine joins the EU, its demand base effectively becomes part of the European demand base. But there is an important nuance here.

Europe is not waiting for Ukrainian grain as a product that will simply replace local production.

There are farmers in Poland. There are farmers in France. There are farmers in Germany. There are also farmers in Hungary, Romania, Bulgaria and Austria.

So Ukraine’s growth has to be complementary to the European economy, not in conflict with it.

Latifundist.com: What does “complementary” mean in practice?

Cesar Soares: It means creating products that Europe needs.

Bioenergy, for example. Europe has huge demand for decarbonization and alternative energy sources. Ukraine has land, raw materials and the potential to produce bioenergy products.

The same applies to animal protein. The same applies to value-added food products.

Today, Ukraine exports wheat to Turkey. Turkey processes it into flour and finished products, and then sells them further.

The logical question is: why is part of that value not created in Ukraine?

Maybe, in time, some of the largest producers of biscuits or pasta will operate in Ukraine and export finished products to Europe and other markets.

Latifundist.com: How much has the war changed this scenario?

Cesar Soares: The war has delayed some of these processes, but it has not canceled them. Yes, some companies lost assets, and some facilities were destroyed. But Ukraine’s agricultural sector was not structurally destroyed.

Ukraine still exports more than 20 million t of corn a year. It remains one of the world’s largest exporters of grains and oilseeds.

So the main post-war discussion is not about rebuilding the sector as such. The main discussion is about what the next model of its development will look like.

Latifundist.com: What kind of Ukraine do you see after the war?

Cesar Soares: It will be a country of reconstruction. A country integrating into the European Union. A country of new investment. And this will especially apply to agriculture.

Ukrainian agriculture has shown such resilience during the war that it will remain one of the key areas of the country’s economic development.

Ukraine has very strong entrepreneurs. This is one of the main reasons for my optimism.

That is why I am convinced that if we have this conversation a few years after the war ends, many things will have changed much faster and on a much larger scale than we can imagine today.

Latifundist.com: If we meet at Grain Ukraine in 2050, what will surprise today’s farmers and agribusiness leaders the most?

Cesar Soares: I think they will be surprised that Ukraine once exported most of its production as raw grain.

Future generations of farmers will find it strange that we used to grow corn or wheat, move it hundreds of kilometers to the port, and have almost no domestic demand for that product.

To me, this may become one of the biggest historical paradoxes of Ukrainian agriculture.

Africa: a future market or a future competitor?

Latifundist.com: You often call Africa one of the main stories of the coming decades. Do you see Africa primarily as a center of future demand, or as a future competitor for today’s agricultural exporters?

Cesar Soares: Africa has hundreds of millions of hectares of land suitable for farming, and around 60–65% of all unused arable land in the world. But first, we need to avoid one mistake: there is no single Africa.

Talking about Africa as one homogeneous market is a bit like talking about Asia as one country. The continent is extremely diverse — economically, politically and culturally.

This is also clear from import data. According to UNCTAD’s The State of Commodity Dependence 2025 report, Africa’s food imports in 2021–2023 were estimated at $97 billion, but the largest volumes were concentrated in North African countries: Egypt, Algeria and Morocco.

But if we look at it strategically, my main point is this: if Africa’s population really grows the way the UN projects, this will only be possible through a sharp increase in its own agricultural production.

Latifundist.com: Why not through imports?

Cesar Soares: Because the infrastructure simply will not be enough.

Today, Africa’s population is around 1.5 billion people. If it grows to 2.5 billion, the continent will have to feed roughly one billion more people.

Based on my own calculation in grain equivalent: if Africa’s population rises to 2.5 billion and average consumption reaches 300 kg in wheat or corn equivalent per person per year, the continent’s total need could reach around 750 million t. This is not an official forecast. It is a way to show the scale: future demand growth will be much larger than today’s import volumes.

So doing this through imports would be practically impossible. There will not be enough ports, railways or logistics corridors. If this demographic scenario comes true, Africa will have to increase its own production.

Forbes Africa has written about the same problem: Africa imports more than $50 billion worth of food every year, which makes it especially vulnerable to grain shocks, trade conflicts and price volatility. The outlet sees the way out not only in increasing production, but also in innovation and the development of intra-African trade.

Latifundist.com: So Africa will gradually turn into a major agricultural producer?

Cesar Soares: Exactly. And this is where another important factor comes in: technology.

Many African countries are gaining access to tools that were not available before: artificial intelligence, digital services, mobile platforms and modern agronomy.

Some countries even have the advantage of not being burdened by outdated infrastructure. Kenya is a good example. It moved directly into mobile technologies, skipping many intermediate stages of development.

In a way, the same thing may happen in agriculture. So I do not rule out that Africa’s production growth potential is seriously underestimated today.

Read also: Beyond grain: how Ridne launched an agri-food hub in Ghana, competes with Russians in Africa and builds partnerships with local farmers

Latifundist.com: So is Africa a threat to Ukraine?

Cesar Soares: No. I see it as an opportunity.

Even if Africa increases its own production, it will still need technologies, food products, bioenergy solutions, investment and processed products.

This is where an opportunity opens up for Ukraine. I think it is quite realistic that in 20–30 years, Ukraine will sell Africa not grain, but highly processed products: pasta, bioenergy solutions and biochemical products.

In other words, the potential market for Ukrainian goods in Africa is much larger than the potential market for Ukrainian raw materials. So I do not see Africa as Ukraine’s competitor. I see it as one of the most interesting markets of the future.

China, bioenergy and the new geography of demand

Latifundist.com: You have said several times that China may gradually reduce its dependence on imports of grains and oilseeds. How realistic is this scenario?

Cesar Soares: In my view, this is one of the most important trends of the coming decades.

China is a classic example of an economy where demographic growth no longer works as a demand driver. China’s population is already shrinking. In Shanghai, the total fertility rate is around 0.6 children per woman — one of the lowest levels in the world. Urbanization is also slowing down. This means that one of the key factors that supported the growth of agricultural imports for many years is gradually weakening.

At the same time, China is actively investing in its own production. China harvests almost 300 million t of corn every year. A few decades ago, these numbers were much lower.

If we look more broadly at grains and oilseeds, China’s production has grown from 260 million t in 2000 to 460 million t. China is not just a major importer. It is also building an increasingly strong domestic production base.

So we see two trends at the same time: domestic production is growing, while demand is reaching a plateau.

Latifundist.com: Does this mean China will stop being the main driver of global imports?

Cesar Soares: I do not think this will happen tomorrow. But in the long term, this is where things are heading. Especially when it comes to corn.

For many years, China has been encouraging the growth of domestic production. The approval of GM corn was one of the most important signals showing how seriously the country takes food self-sufficiency.

The same is happening in oilseeds. The Chinese government openly talks about the need to reduce dependence on soybean and soybean meal imports.

Latifundist.com: We often hear that China simply has no alternative to imports.

Cesar Soares: I would not agree with that. China does not think only in terms of food. It thinks in terms of security: food security, energy security and control over critical infrastructure.

That is exactly why China wants to produce more at home.

Look at energy. China remains one of the world’s largest energy importers. For an economy of this size, that is a strategic vulnerability.

So bioethanol becomes more than an agricultural story. It becomes an element of national security.

Latifundist.com: So China could repeat the path you are suggesting for Ukraine?

Cesar Soares: Partly, yes. China also has corn, and China also needs energy. It also has a political motivation to reduce dependence on external suppliers. So the development of bioethanol looks like a very logical direction.

That is why I do not see China as the future driver of global grain imports. I see it more as a country that will gradually increase its own production of food and energy.

Why Brazil needs to watch China closely

Latifundist.com: If China really starts importing less, who will feel it the most?

Cesar Soares: Brazil, first of all. Today, China is the key buyer of Brazilian soybeans. Brazil has built a huge part of its agricultural success around Chinese demand.

The scale of this story is clear in the numbers: between 2000 and 2025, Brazil’s grains and oilseeds production grew by 466%, while corn yields increased by 103%. So Brazil did not simply benefit from Chinese demand — it rebuilt its agricultural model around it.

That is why any structural change in China automatically becomes a strategic issue for Brazil.

Latifundist.com: Is Brazil ready for that scenario?

Cesar Soares: Well, it has already started adapting.

One example is the development of corn ethanol. Brazil is gradually building its own bioenergy industry and has every chance of becoming one of the world’s largest ethanol exporters.

In fact, it is already starting to do the same thing we are talking about for Ukraine: creating new markets for its own agricultural production.

Why bioenergy is becoming critical for agriculture

Latifundist.com: Bioenergy often sparks debate. Critics say fuel competes with food.

Cesar Soares: In the past, that argument made sense. When the world’s population was growing quickly and production could not keep up with demand, one could argue that grain should be used primarily to feed people.

But today, the situation is changing. We are moving into a world where technology continues to increase production faster than demand grows.

And if we do not find new ways to use grains and oilseeds, we risk facing a different problem: a lack of economic incentives for further production growth.

The paradox is that food security in the future may depend precisely on how successfully we create additional demand for agricultural products outside the food sector.

The main challenge of the future is not to grow more grain

Latifundist.com: If you had to sum up our conversation in one conclusion, what would it be?

Cesar Soares: For decades, agriculture mostly answered one question: how do we produce more? I think the coming decades will be about a different question: what do we do with what we have produced?

Over the past 25 years, the world went through a stage of massive expansion: population grew by 34%, grains and oilseeds production by 47%, exports by 118%, and biofuel use by 844%. But these numbers show the change in logic: the future of agriculture will be defined not only by the ability to grow more, but by the ability to create demand for what can already be grown.

The world will continue to increase yields. Technology will continue to improve efficiency. Artificial intelligence will speed up many processes. So the main challenge will be creating demand.

The future will belong to countries and companies that learn not just how to grow grain, but how to create new ways to use it.

And that is why I believe Ukraine has a unique chance to become one of the main beneficiaries of this transformation.