When soybeans become fuel: South America’s biodiesel factor — ASAP Agri

Biodiesel has already become a key pillar supporting soybean demand and prices in the U.S. But the global balance is shaped just as much by developments in South America — the region that dominates global soybean supply, says Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri.

Brazil: demand is shifting inward

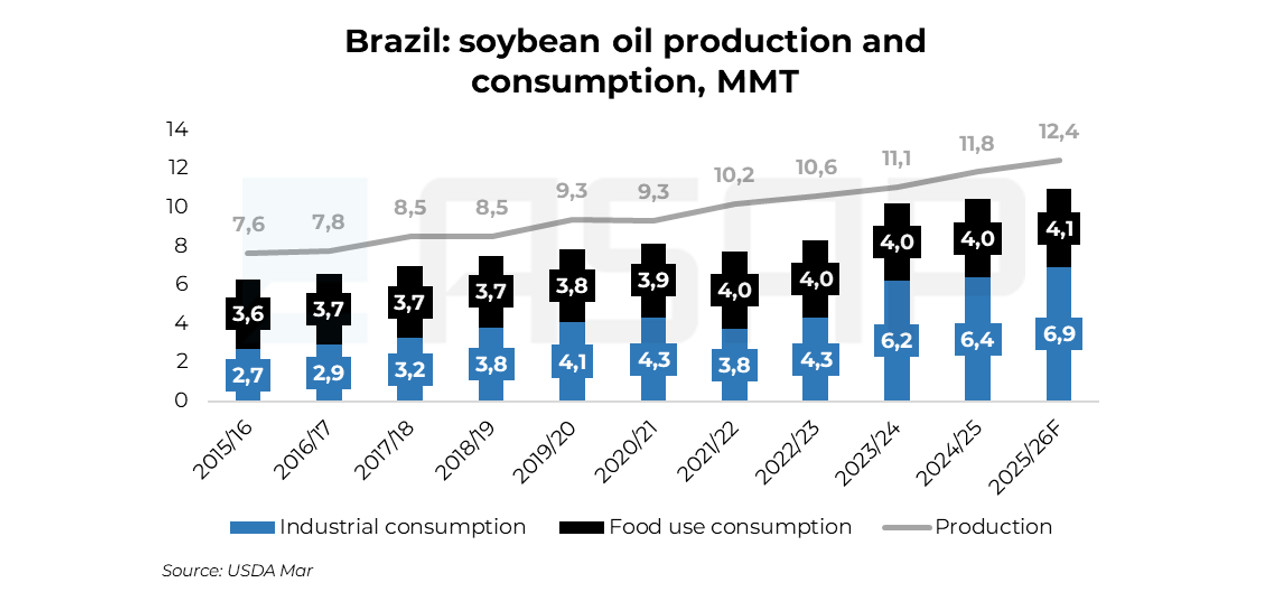

Brazil is emerging as a second major source of demand growth for soybean oil, driven by the steady expansion of its biodiesel sector. After a pause during the energy crisis, the country resumed raising blending mandates, increasing the requirement from B14 to B15 in August 2025.

Around three-quarters of Brazil’s biodiesel is produced from soybean oil, linking the sector directly to soybean demand. Each additional percentage point in the mandate requires roughly 400 KMT of soybean oil, making policy changes immediately visible in the balance sheet.

That shift is already reflected in the data. Soybean oil production is projected to reach 12.44 MMt in 2025/26, while industrial use — including biodiesel — is expected to rise to 6.9 MMT, up sharply from 4.3 MMT in 2022/23.

Yet the next step remains uncertain.

Brazil’s Fuel of the Future framework outlines a gradual increase in biodiesel blending to B20 by 2030, but implementation depends on technical validation and approval by the National Energy Policy Council (CNPE). The planned move to B16 in March 2026 did not materialize, leaving the mandate at B15.

As of mid-March, technical trials had yet to begin, and the CNPE meeting expected to decide on the increase was canceled without a new date.

The base case now points to B15 remaining in place through most of 2026, with a possible shift to B16 later in the year — or beyond. Some market participants do not rule out delays into 2027.

Political caution is also playing a role. With elections approaching, the government is wary of measures that could push up diesel prices or add to inflation, even as biodiesel producers continue to lobby for higher mandates.

The result is a market where demand continues to grow, but at a slower and less predictable pace than previously expected. Domestic consumption remains an important pillar, though its expansion is becoming more gradual.

Argentina: capacity without demand

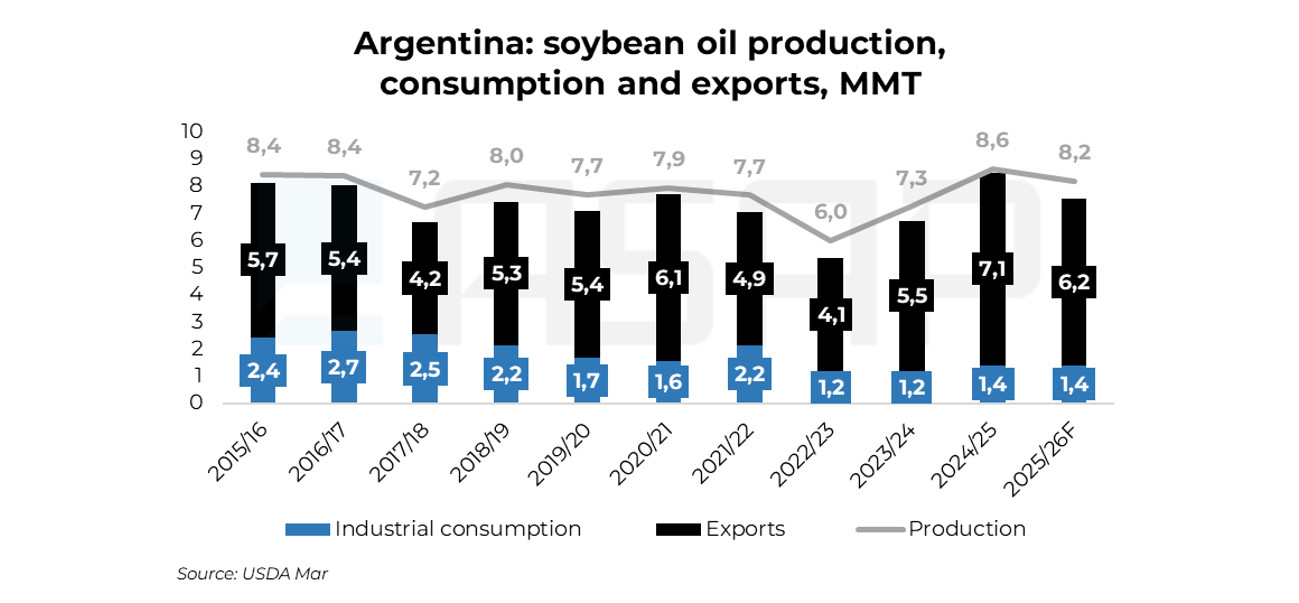

In contrast, biodiesel has yet to become a meaningful driver of domestic demand in Argentina.

Despite operating one of the world’s largest soybean processing industries, the country’s internal consumption of soybean oil remains limited. Industrial use, including biodiesel, is estimated at around 1.4 MMT in 2025/26 — only marginally above recent seasons and well below levels seen a decade ago.

The sector is running far below capacity. Biodiesel production is estimated at 1.2–1.3 BLN L in 2025, compared with installed capacity exceeding 4.4 BLN L.

Policy remains the key constraint.

While the official blending mandate is set at 7.5% through 2030 — with 5% reserved for smaller producers — the government has repeatedly adjusted effective blending levels to manage fuel prices. In November 2025, the mandate was temporarily reduced to 7% to contain diesel costs.

Even when formally restored, actual blending often falls short of the official target due to price controls and excess capacity.

As a result, roughly 70% of Argentina’s soybean oil output continues to be exported. This reinforces the country’s role as a major global supplier but limits the development of its domestic biodiesel market.

Although expansion plans exist, policy direction remains cautious. The government is focused on controlling inflation, boosting domestic oil and gas production, and reducing reliance on diesel imports.

Under these conditions, biodiesel provides only limited support to domestic soybean oil demand — and falls well short of the role it plays in Brazil.