Rapeseed: sell or wait? What Euronext is signaling — ASAP Agri

The Euronext rapeseed market continues to show resilience. Despite the recent correction across related oilseed and grain markets, the August contract has spent recent weeks consolidating within a relatively narrow range of 520–530 EUR/MT.

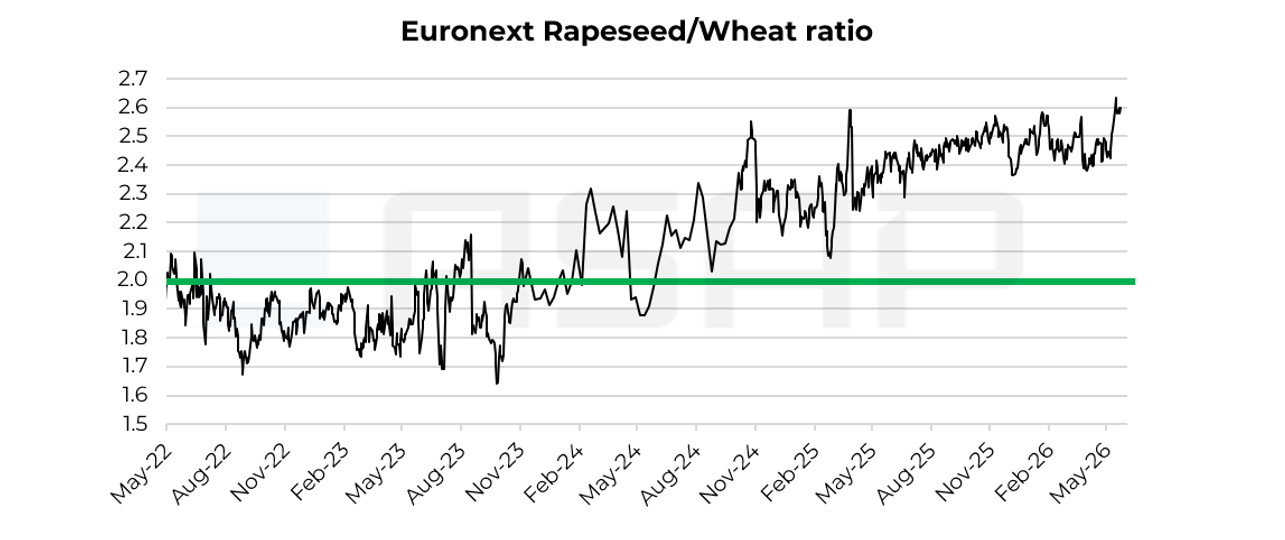

At the same time, the Euronext rapeseed-to-wheat ratio climbed to 2.6 in June, well above its historical norm of around 2.0, says Head of Editorial, Content and Analytics at ASAP Agri Victoria Blazhko.

Notably, the ratio has remained firmly within the 2.3–2.6 range over the past year. This substantial premium of rapeseed over wheat reflects two key factors.

On the one hand, the global wheat market remains well supplied following last season’s record harvest, limiting upside potential for grain prices. On the other hand, the rapeseed complex continues to benefit from strong support from the biofuels sector. Rapeseed oil remains the primary feedstock for biodiesel production in the EU, while the implementation of RED III and the gradual phase-out of palm oil provide additional support to demand.

Another important factor is the EU’s structural deficit in rapeseed. Domestic production remains insufficient to fully utilize crushing capacity, leaving the bloc dependent on imports, primarily from Ukraine, Australia, and Canada.

As a result, European crushers remain willing to pay a premium for rapeseed, allowing the crop to trade significantly above wheat for an extended period.

However, despite the supportive fundamentals, the current ratio is hovering near the upper end of its multi-year range. A high ratio is not, by itself, a signal of an imminent correction. Yet the higher it climbs, the more dependent the market becomes on further gains in rapeseed oil prices and the preservation of healthy crushing margins in Europe. Without fresh demand-side catalysts, the scope for additional upside appears increasingly limited.

Seasonality may work against the market

Seasonal factors are emerging as an additional source of risk.

The August Euronext contract is currently trading 40–60 EUR/MT above levels seen at this time of year over the past three seasons. Historically, July through August has often marked a correction phase following spring and early-summer rallies as new-crop supplies enter the market.

The technical picture also points to a loss of upward momentum. Several attempts to establish a foothold above 530 EUR/MT have failed, highlighting strong resistance at those levels and limited willingness among buyers to push prices materially higher.

What to expect in July–August

The combination of seasonal factors, an elevated rapeseed-to-wheat ratio, and the current technical setup suggests that near-term risks are gradually shifting toward a correction.

Key drivers could include the arrival of new-crop supplies in both the EU and Ukraine, seasonally slower purchasing activity by crushers, and profit-taking by investment funds following the recent rally.

Additional pressure may come from a relatively comfortable supply outlook in Europe. Most analysts project EU rapeseed production in 2026/27 at 20–21 MMT, broadly in line with or only slightly below the previous season and still above the five-year average. In other words, the market is entering the new season without significant supply concerns.

Under this scenario, the August contract could correct toward 500–510 EUR/MT. If weather conditions remain favourable and harvest results in both the EU and Ukraine meet expectations, a test of 480–490 EUR/MT cannot be ruled out.

At the same time, a deeper decline currently appears unlikely. Structural demand from the biofuels sector continues to provide substantial support and should help limit downside potential.

What does this mean for Ukraine?

Current conditions in the physical market remain favourable for Ukrainian rapeseed sellers. This is clearly reflected in the basis: the spread between Ukrainian rapeseed prices on a CPT-port basis and the August Euronext futures contract currently stands at just -6 USD/MT, one of the strongest levels typically seen at this stage of the season.

Historically, such a strong basis rarely persists for long. Once harvest pressure intensifies, the basis tends to weaken.

Taken together, the market is sending several signals at once: rapeseed is trading at an unusually high premium to wheat, the August futures contract remains near the upper end of its multi-year range, and the Ukrainian basis is exceptionally strong. Combined, these factors create a favourable window for locking in part of new-crop sales.