Five Key Extremes Behind Ukraine’s Agricultural 2025 — ASAP Agri Year Review

Photo by: Latifundist.com

ASAP Agri sums up the agricultural year 2025 — a season that for Ukraine’s agribusiness looked more like an obstacle course than a smooth run. According to the Eastern calendar, it was the Year of the Green Wooden Snake — a symbol of flexibility and the ability to change trajectory quietly. That is exactly how the season unfolded: without sharp moves, but with a constant need to adapt and rebuild strategies on the go.

The market spoke the language of fields, ports, and exchanges — a language we analyzed in detail throughout the year in ASAP Agri’s analytics, including our regular blog on Latifundist.com. Now, we bring the full picture together.

Weather extremes: from drought to rain

The first major blow of the season came from the weather. Drought in Ukraine sharply reduced the potential of spring crops, especially oilseeds. According to ASAP Agri estimates, the 2025 sunflower harvest fell to 10.4 MMT — a ten-year low, down from 12.1 MMT last year. This clearly reflects the depth of weather stress in key producing regions.

The second act came with rain during harvesting. They delayed fieldwork and postponed market arrivals for both winter and spring crops. As a result, the 2025/26 season started slowly, but instead of the usual harvest pressure, the market saw atypical support for domestic prices.

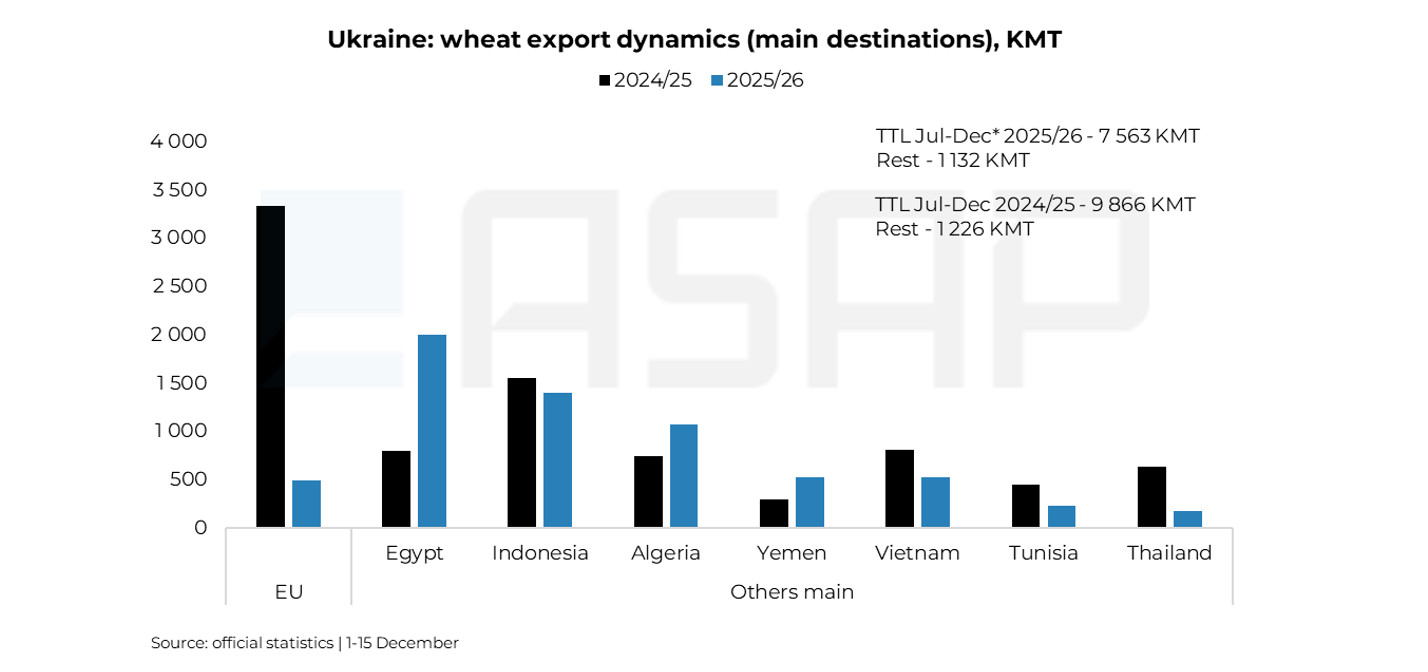

European extremes: from trade visa-free to quotas

The second defining factor of 2025 was the return of EU import restrictions on Ukrainian grain. After russia’s full-scale invasion in 2022, the EU granted Ukraine a “trade visa-free” regime, effectively removing grain tariffs and quotas. But in 2025, the EU — Ukraine’s largest grain buyer — reverted to a quota-based system.

From 6 June 2025, annual tariff quotas were reinstated: 1 MMT for wheat, increased to 1.3 MMT from late October; around 450 KMT for barley (up from 350 KMT previously); and up to 1 MMT for corn, increased from 650 KMT, although the quota impact here was minimal due to zero tariffs.

The hardest hit was wheat. In July–November 2025, exports to the EU fell to 490 KMT from 3.1 MMT a year earlier. This means this season Ukraine must redirect 3–3.5 MMT of wheat to alternative markets — a highly challenging task amid record global harvests and abundant supply.

Regulatory extremes: from exports to processing

The third turning point was the so-called rapeseed–soybean amendments. The introduction of a 10% export duty from 4 September sharply slowed exports at the start of the season. Due to unresolved procedures for duty exemptions for producers, part of the market effectively “froze,” and soy and rapeseed exports were disrupted during peak months.

Rapeseed exports in July–November more than halved y/y, while soybean exports in September–November dropped nearly threefold. At the same time, regulatory changes shifted the focus toward domestic crushing. For the first time in Ukraine’s history, rapeseed and soy processing is not only catching up with exports but starting to overtake them.

Against ASAP Agri’s forecast of a reduced sunflower crop at 10.4 MMT, processing capacity exceeding 20 MMT per year looks more underutilized than ever. Plants are actively seeking alternative feedstock, with rapeseed and soybean partly filling the gap. As a result, 2025/26 may become a historic season: rapeseed processing could rise to 1.4 MMT (from 490 KMT last year), while soybean processing may reach 3 MMT, surpassing exports for the first time (exports estimated by ASAP Agri at 2.2 MMT).

Logistics extremes: from active shipments to standstills

The fourth factor that has prevented the Ukrainian market from “catching its breath” for months is chronic logistics disruption. These problems began forming in October and sharply worsened toward year-end amid massive russian attacks on energy, rail, and port infrastructure. Logistics became a key price driver. At the Greater Odesa ports — Pivdennyi, Odesa, and Chornomorsk — power outages, generator-only operations, and constant air-raid alerts significantly reduced throughput. Formally open ports increasingly operate in a stop-start mode.

Rail logistics also became more complex and expensive: locomotive shortages, wagon delivery restrictions, slow truck unloading, and rising operational risks effectively narrowed the export corridor. The market once again saw the 2022 scenario: grain is available domestically, but physically delivering it to buyers is increasingly difficult. This supported CPT prices from October, but by year-end, the factor began working against price growth, as excessive risks and contract execution uncertainty pushed some players to step aside. Delivering grain to port has become a quest.

According to ASAP Agri, without stabilization of Ukraine’s security situation, logistics constraints are likely to persist until the end of winter, restraining exports and increasing the risk of high carry-over stocks, especially corn, at the start of the 2026/27 MY.

Global extremes: from balance to surplus

The fifth — external but no less decisive — factor was the record global supply of grains and oilseeds in 2025/26. According to the USDA, global wheat production reached a historic 837.8 MMT, while corn output hit a record 1283 MMT. Oilseed supply also remains excessive: soybeans at 422.5 MMT and rapeseed at 95.3 MMT, near or at historical highs.

This volume created a surplus market with extremely fierce competition among exporters and limited upside for prices. The second half of 2025 clearly showed that lower prices win in global trade — and increasingly, the combination of price, logistics, and risk, which under current conditions puts particular pressure on Ukraine, especially in wheat and corn markets.

With this baggage — record global supply, intense competition, and vulnerable Ukrainian export logistics — Ukraine’s agricultural market enters 2026, the Year of the Fire Horse. It will be a season of speed, sharp moves, and high stakes, where winners will not be those waiting for the perfect moment, but those who see signals in time, understand market logic, and act ahead of the curve.

That is exactly why the ASAP Agri team works daily with data, flows, and context — so analytics become a decision-making tool, not just a set of numbers. If it matters not only to follow the market but to understand where it is going and why, stay within our information space and subscribe to ASAP Agri analytics.

May the Year 2026 be dynamic yet predictable — and your decisions timely and well-balanced.

Victoria Blazhko, Head of Editorial, Content & Analytics at ASAP Agri