Ukraine faces rising carry-over grain stocks as export pace weakens in 2025/26 — ASAP Agri

Ukraine’s 2025/26 grain export season began with a noticeable slowdown. A delayed harvest, logistics disruptions, and regular russian strikes on rail, energy, and port infrastructure are knocking out the very period when Ukraine traditionally ships the bulk of its grain, says Victoria Blazhko, Head of Editorial, Content and Analytics at ASAP Agri.

Shipment pace over the summer and autumn lagged behind normal levels, and winter is unlikely to bring relief. This is pushing the market toward the largest carry-over stocks in years and shaping not only the current season, but the next one as well.

Wheat: a 1.5 MMT export shortfall already

Between July and November, Ukraine exported 7.3 MMT of wheat, compared with 9 MMT a year earlier. The sharpest decline came in July, when delays in harvesting cut shipments by half.

Typically, the first five months of the season account for around 60% of annual wheat exports. Based on ASAP Agri’s 2025/26 forecast of 14.7 MMT, this would imply about 8.8 MMT. Instead, actual exports undershot by 1.5 MMT — a significant gap for the first half of the season.

Victoria Blazhko

Head of Editorial, Content and Analytics at ASAP Agri

"Closing this gap quickly will be difficult. Winter logistics are unlikely to improve meaningfully; the global market is oversupplied, and EU quotas continue to restrict access for Ukrainian wheat. Meanwhile, Argentina and Australia are entering the global market with record crops, drawing away key demand."

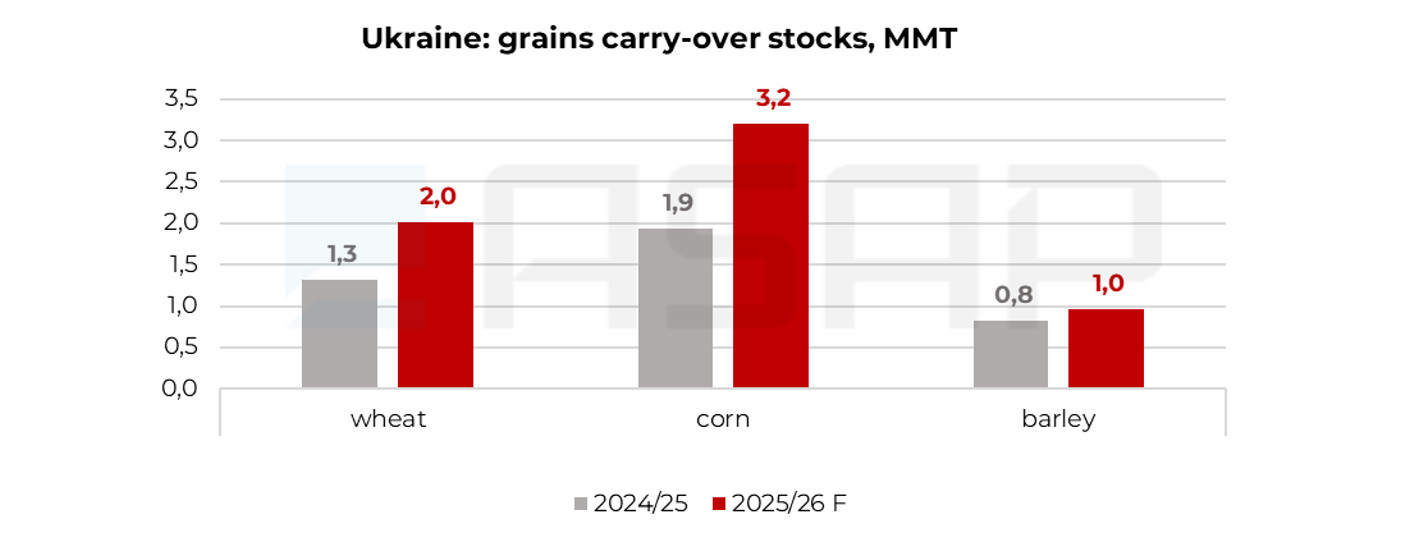

As a result, wheat carry-over stocks in 2025/26 could rise to 2 MMT — the highest since 2022/23. And even this forecast may prove conservative if the 1.5 MMT export gap is not offset in the second half of the season.

Corn: 3 MMT in carry-over — basic scenario

The situation in corn looks even more strained. In October–November, Ukraine exported 2.8 MMT versus 4.5 MMT last year. According to ASAP Agri estimates, the base-case forecast for 2025/26 corn exports stands at 22 MMT, based on a reduced production estimate of 29.3 MMT reflecting the most recent field data. A pessimistic scenario — increasingly realistic — suggests exports could fall to 20 MMT.

Ukrainian export corn prices have been trending lower in recent days, improving competitiveness on some markets. However, demand on key destinations remains weak: the U.S. is offering large volumes, and competition from South America typically intensifies in the second half of the season.

This makes the winter period decisive. In December–February, Ukraine usually ships around 35% of its annual corn exports. To meet ASAP Agri’s base-case forecast of 22 MMT, at least 7.7 MMT must be exported during these three months — roughly 2.6 MMT per month. Given current logistical constraints and sluggish demand, this is a high bar, though still achievable.

Under the base scenario, corn carry-over stocks in 2025/26 could rise to 3 MMT — 1 MMT more than last year, marking the highest level since 2021/22. Under a pessimistic scenario, up to an additional 2 MMT could be added.

Thus, Ukraine enters the middle of the 2025/26 season with unprecedented risks of grain accumulation. The main pressure comes from wheat and corn — the core of the export balance.

If winter logistics do not stabilise and demand in key markets does not strengthen, the season may end with the largest carry-over stocks in the past three years — a direct path to increased pressure on domestic prices in the longer term.