Despite the fact that the total export of agricultural products from the USA in 2019 exceeded the Ukrainian one by 6 times, its share in the gross export is only 8.2%. (For comparison, in Ukraine this figure is 44.2%). The largest position in the structure of US agricultural exports is soybeans with market sales of $ 17.0 billion. At the same time, soybeans occupy only 12th place in the structure of exports of all goods from the United States. In the top ten of high-tech products are electronics, airplanes, electric vehicles, etc.

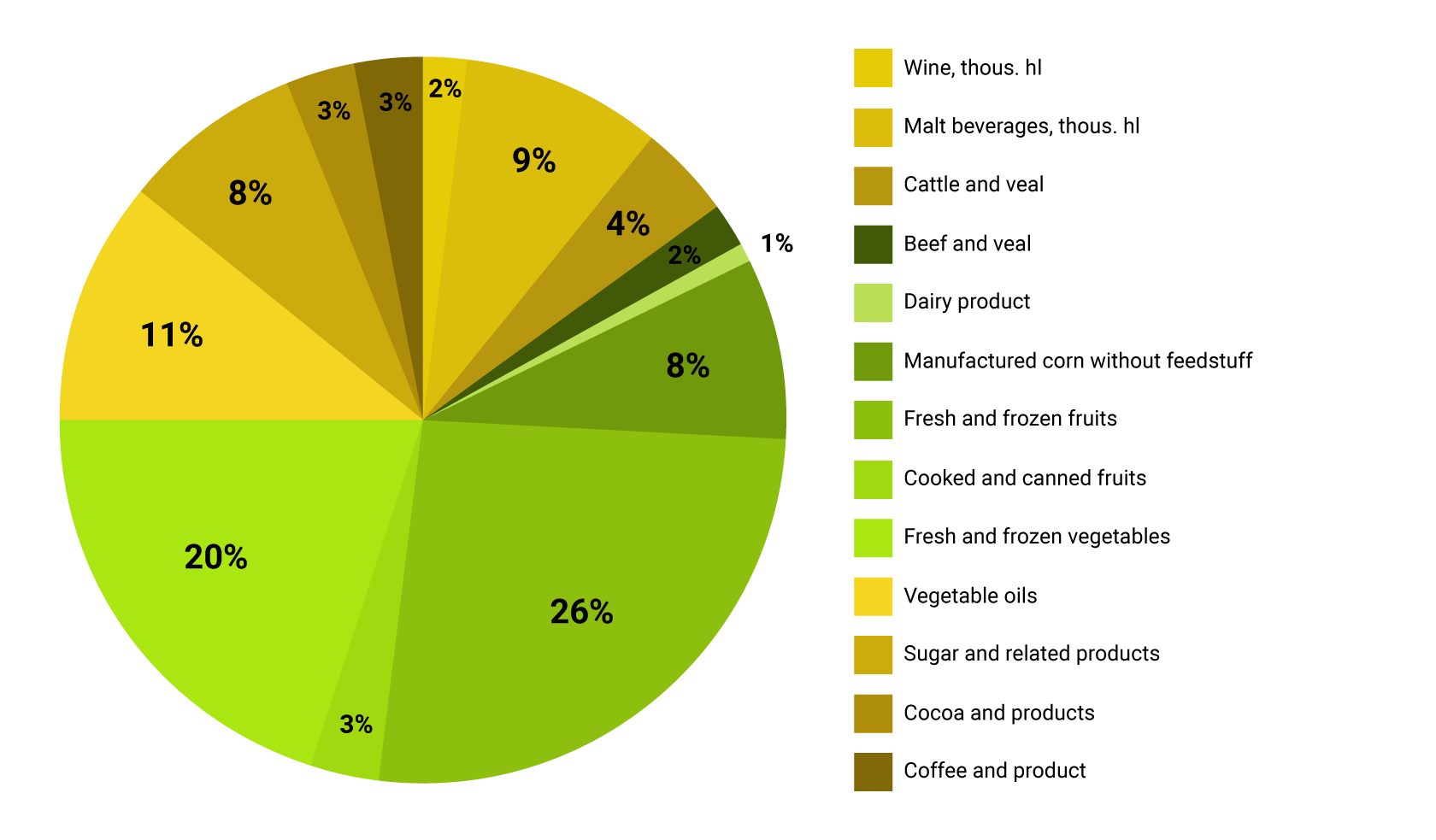

According to the data of the State Customs Service, the TOP-5 export positions in Ukraine looks like this:

In the United States, the bulk of government agricultural support programs are carried out through the Commodity Credit Corporation and the Farm Service Agency, which are structural divisions of the United States Department of Agriculture (USDA). Through its structural divisions, the USDA implements several dozen programs aimed at supporting farming activities, stimulating exports, preserving the environment, careful use of soil, supporting the production of certain types of products, etc.

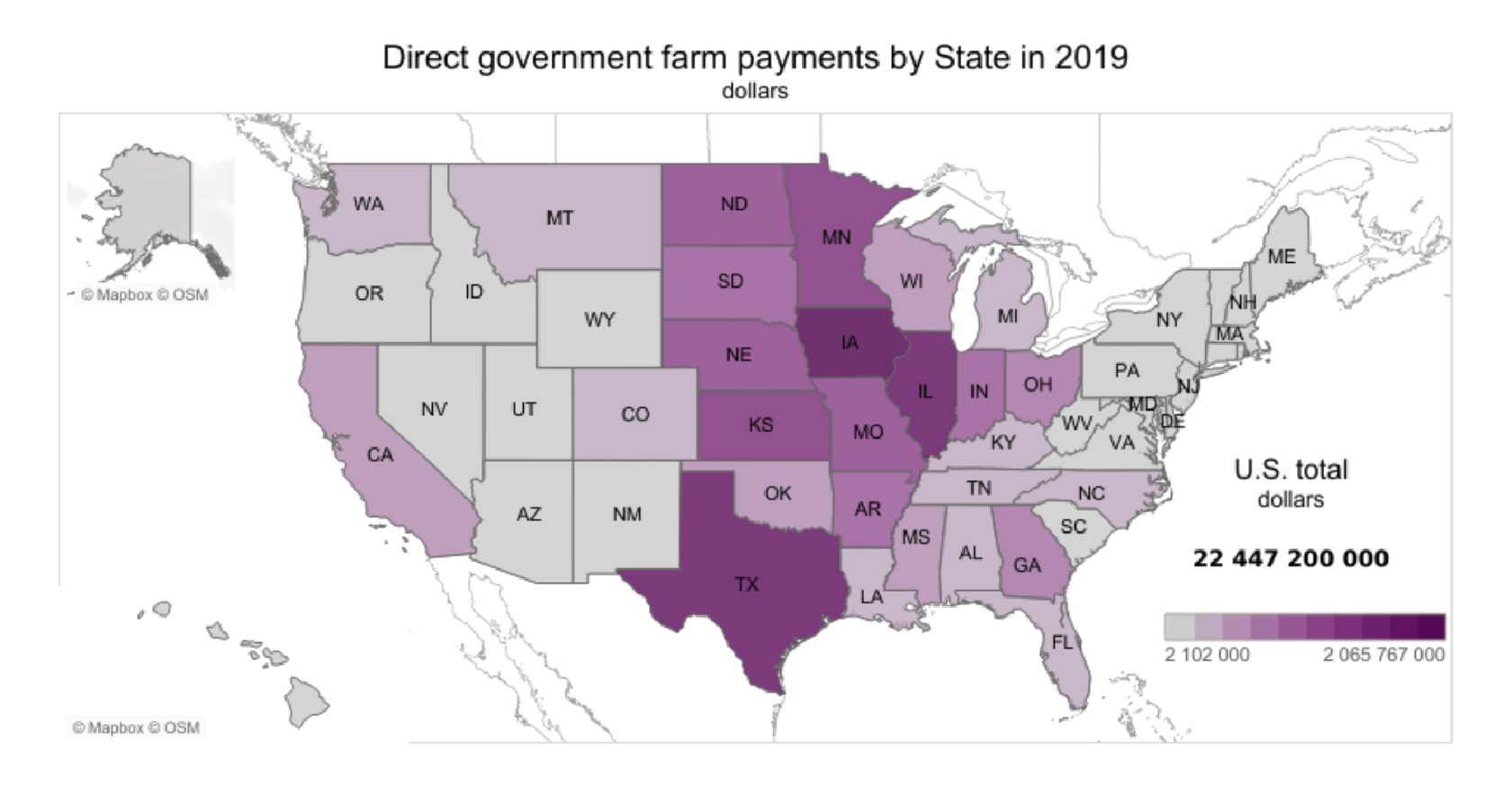

In 2019, the US government allocated $ 22.4 billion to support the agro-industrial complex, which is 63.5% more than in 2018. According to preliminary estimates, in 2020, the total amount of state support for the American agricultural sector will amount to $ 44.5 billion (an increase 98.7%). The increase in the amount of state support by 2.2 times was due to an increase in expenditures for two programs: